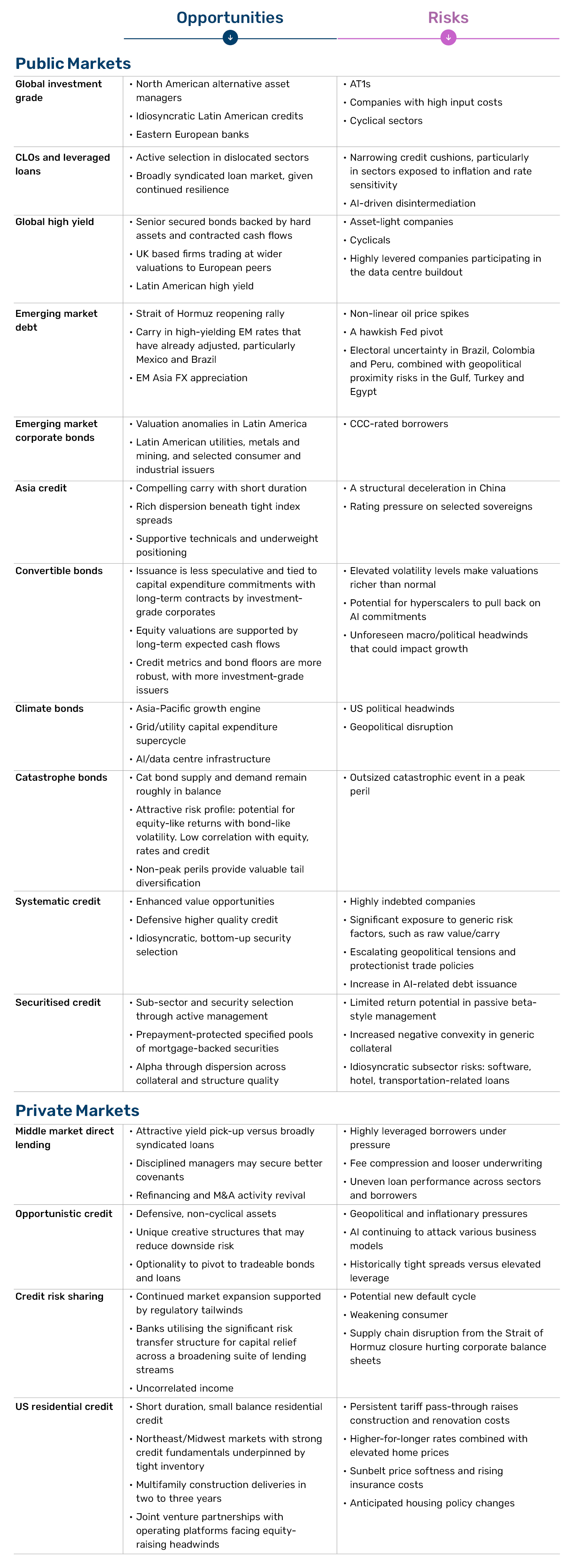

In focus

The Gulf conflict has understandably dominated headlines in recent months, but credit markets have had another story to tell. Artificial intelligence (AI) and hyperscaler bond issuance is booming in public markets, while in private credit, a series of high-profile defaults has placed AI and software deals under the microscope.

In light of these developments, we are devoting this section of the credit outlook to AI and its growing footprint across public and private credit markets. The regular sector outlooks follow below. We also offer a snapshot of how we are using AI to advance our credit capabilities.

AI bond boom

The pace of bond issuance in the AI and hyperscaler space year to date has been nothing short of staggering – and expectations only point to an acceleration in the coming quarters.

Figure 1: AI-driven issuance is surging

Problems loading this infographic? - Please click here

Source: Dealogic, Pitchbook | LCD, Morgan Stanley Research forecasts, as of May 2026.

As a point of comparison, internet and tech issuance during the dot-com era peaked at US$85 billion in 2001, representing an average of 14.5% of total issuance across 2000–2001. The current cycle threatens to dwarf that period: at the high end, Morgan Stanley estimates total AI and hyperscaler-related issuance could reach US$400 billion in investment grade (IG) and a further US$65 billion in high yield and loans, potentially accounting for nearly 20% of total issuance. Bear in mind that, at the start of 2015, the hyperscalers (Amazon, Microsoft, Meta, Alphabet and Oracle) represented less than 1% of the market.

Figure 2. The dot-com bubble had nothing on today's AI supply boom

Problems loading this infographic? - Please click here

Source: Dealogic, Pitchbook | LCD, Morgan Stanley Research forecasts, as of May 2026.

Feeling the weight

Credit markets are already feeling the weight of that supply. Year to date, four of the five hyperscalers have underperformed the broader market on a spread basis.1 The scale of AI-related capital expenditure (capex) is also impacting US GDP, where economists forecast a contribution of around 1% in 2026,2 potentially papering over cracks elsewhere. Despite spread widening, we do not believe levels adequately compensate investors for the risks given the supply overhang and, in our view, growing concerns around competition, buildout delays fuelled by labour shortages, increased public backlash and regulatory intervention.

Coiling the spring

While supply alone is not necessarily sufficient to trigger a broad sell-off, the sheer scale of forthcoming paper risks pushing spreads wider across the credit complex. The substitution effect is a key transmission mechanism: as investors are required to absorb ever-larger volumes of higher quality AI-related supply (and Treasuries to finance fiscal deficits), compensation in the form of wider spreads across lower quality issuers becomes increasingly necessary to clear the market.

While many of these deals benefit from robust structural protections including amortisation features, construction guarantees, and hyperscaler lease backstops, the enthusiasm for the sector has encouraged significant overreach. We believe investor caution is warranted given the execution risk inherent in such a rapid buildout: capital intensity has not yet peaked, off-balance sheet leverage is rising, and sustainability of returns on AI investment remains unproven, particularly for neo cloud and data centre operators further down the credit quality spectrum.

We are particularly concerned about issuance in the high yield and leveraged loan markets, where many borrowers remain firmly free-cash-flow negative.

Figure 3. Software's footprint in leveraged loans has soared

Problems loading this infographic? - Please click here

Source: JP Morgan, as of 9 June 2026.

History rhymes

Sector vulnerabilities are not new to credit markets. Recall the mini cycles in internet and telecoms in the early 2000s, European sovereigns and banks in 2012, energy in 2015-2016 and real estate/cyclicals in 2022. Stress rarely discriminates within vulnerable sectors, but this might create opportunities to buy the best houses in the worst neighbourhoods. For now, we have been focusing on software companies with stronger ties to healthcare and government projects, where margins – while under pressure – remain defensible and refinancing within maturity timeframes appears achievable. Despite all-in spreads remaining expensive, we are seeing signs of dispersion, which we expect to create opportunities.

Figure 4: Dispersion: buy the best house in the worst neighbourhood

Problems loading this infographic? - Please click here

Source: ICE BofA, Bloomberg, Man Group analysis, as of 30 April 2026.

Private credit: deals under the microscope

The dispersion visible in public markets is arguably more pronounced in private credit. A series of high-profile defaults in software and software as a service (SaaS) has placed the sector under the microscope amid comparisons to the dot-com era and growing fears that infrastructure investments could be leapfrogged by newer technologies. Retail outflows, influenced by these concerns, have been portrayed in the media as the beginning of the end of private credit. We prefer to characterise these events as growing pains for the asset class, though credit quality and disciplined manager selection will remain paramount.

When assessing the tech and software portion of the market, which today represents roughly 20% of the middle market direct lending universe,3 we believe a nuanced approach is important. The key distinction is between businesses that are deploying AI to enhance and entrench their competitive position versus those whose core product is being displaced by it. Mission-critical enterprise software with deep customer integrations, high switching costs, and strong pricing power is a very different credit proposition than a point-solution, commoditised SaaS product.

Not all software will face existential disruption, and indiscriminate avoidance of the sector is as much a mistake as indiscriminate concentration within it. The question is whether the borrower is ahead of the curve on AI adoption – using it to widen its moat – or behind it, facing margin pressure and customer attrition.

Last word

Public market credit investors in the AI space face an uncomfortable asymmetry: they bear meaningful exposure to execution risk and buildout delays, yet receive none of the equity upside if the boom plays out as bulls expect. That mispricing of risk is coiling a spring: the greater the enthusiasm today, the more violent the eventual correction is likely to be.

With that said, we are not advocating avoidance. What we believe is required is rigorous credit selection across public and private markets, a clear-eyed view of which borrowers are ahead of the AI curve, and a portfolio that is diversified enough not to be held hostage to the AI story playing out as expected. For investors seeking broader diversification away from the boom, European and emerging market credit might offer an increasingly compelling alternative.

1. As of 8 June 2026.

2. Source: Morgan Stanley, as of 31 May 2026.

3. Source: Pitchbook – “Peek under the Hood: An analysis of private credit loans in top public BDCs”, 28 April 2026.

No paper on AI would be complete without some perspective on how it is changing our day-to-day credit analysis. Below, we describe one of the many tools we have built to improve the quality and efficiency of our research process.

Business development companies present a particular analytical challenge. Their portfolios are typically large, heterogeneous and reported with a lag, making it difficult to identify stress before it surfaces in headline numbers.

Our AI-driven monitoring framework aims to address this by tracking payment-in-kind (PIK) activity, distinguishing loans structured as PIK from inception from those that toggle mid-life, with the latter signalling deterioration. It also aims to detect synthetic PIK, where companies quietly defer cash interest in ways that standard filings do not capture.

In addition, a dedicated module scores every portfolio company on AI disruption exposure and adaptive capacity, identifying which lenders carry the most concentrated risk to AI-vulnerable industries.

Combined with additional signals across sector classification, loan performance and mark migration, the framework seeks to provide an earlier read on distress than public filings alone would allow.

In brief

In depth

At Man Group, we have no house view. Portfolio managers are free to execute their strategies as they see fit within pre-agreed risk limits. With that in mind, click below to expand the outlooks for the second half of 2026 from our different credit teams.

Public markets

Despite the uncertainty of the war in Iran, the first half of the year saw IG credit spreads remain in extremely expensive territory. March inflicted pain on credit investors, with rates and spreads moving higher, but markets have since shrugged off oil price concerns, with valuations at very tight levels of 75 bps of yield above US Treasuries.4 Despite frothy valuations at the index level, opportunities remain for IG investors.

The latter part of 2025 saw hyperscalers tap public bond markets, a theme which has continued into 2026, with players such as Oracle and Alphabet issuing IG-rated notes. Wider newsflow surrounding the impact of AI disruption for SaaS businesses saw Salesforce issue A-rated notes at spreads above the US BBB index. Technology now accounts for 4% of the IG credit market, up from 1% a decade ago.5 Similar market dynamics have also created a spread premium for US business development companies (BDCs), publicly traded entities that fund private credit vehicles.

Given interest rate volatility and geopolitical uncertainty, we do not think now is a time to make significant duration bets. Investment decisions driven by credit selection could help dampen portfolio volatility.

Figure 5: Duration is a tricky game to play

Problems loading this infographic? - Please click here

Source: Bloomberg, as at 26 February 2026, 26 March 2026 and 27 May 2026. Dates selected to capture rate expectations before and during the Iranian war, which began on 28 February.

4. Source: ICE BofA Global Large Cap Corporate Index, as of 31 May 2026.

5. Source: ICE BofA Global Large Cap Corporate Index, as of 31 May 2026.

In our 2026 outlook, we discussed our expectations for continued opportunities within broadly syndicated loans (BSL) against the competing forces of technology and geopolitical risk. Against that backdrop, markets have delivered a varied and volatile path. The war in Iran has constrained supply chains and exacerbated inflationary pressures across Europe, Asia and the US. Inflation, already inflamed by tariff policy, accelerated as corporates struggled to balance a weakening consumer against stretched balance sheets. In February and March, AI developments challenged service and software company valuations. Fears of disintermediation and commoditisation outweighed the promise of efficiency and margin enhancement as debt-laden companies questioned future capital access and revenue streams. What was once a beloved sector and one of the largest exposures within both private and public credit is now a source of uncertainty.

Even so, equity markets hit record highs, benefitting from expanding valuations driven by AI developments. Higher valuations supported wealth effects, offsetting weakness at the lower end of the consumer spectrum. Lower-income consumers, while under persistent pressure, were cushioned by relatively stable labour market conditions.

For BSL, default expectations remain unchanged; retail funds and ETFs continue to report inflows; collateralised loan obligation (CLO) creation resumed after wider liability spreads had temporarily dampened issuance; and earnings continue to find broad support. This is despite limited recovery in sectors more exposed to inflation and rate sensitivity, including housing, building products and packaging. Notably, the largest syndicated leveraged loan since 2007, Warner Brothers Discovery, was sold to investors in May. This US$15 billion syndication ranks second only to the TXU transaction in 2007.

We continue to expect 2026 to reward active investors. Identifying potential winners and losers in fast-moving markets, particularly when refinancing capital structures in unloved sectors, could create opportunities unavailable in a compressing spread environment. Scrutiny is high and patience is low, and we believe these conditions may potentially present an opportunity to outperform.

It is important to monitor narrowing credit cushions, the fragility of the market’s current pillars of strength, and the potential impact of sustained geopolitical conflict on the outlook. These risks are perhaps best captured by three indicators: the US personal savings rate, equity-driven wealth creation and technology’s contribution to equity market performance.

High yield markets have been active in 2026, with US issuance tracking roughly 50% above last year's pace6 and European supply holding up despite periodic volatility.

Returns have been positive but modest, with higher quality BBs and Bs outperforming CCCs, while spreads remain tight by historical standards at around 267 bps in the US and 260 bps in Europe.7

Beneath the surface, dispersion is at record levels, with a growing tail of stressed names trading at deeply discounted levels. Defaults remain contained at roughly 1.8% in European high yield and around 4% in the US, but recovery rates on first lien loans sit well below long-term averages, underscoring the importance of credit selection and structural seniority.

The earnings backdrop is constructive and broad based, with consensus estimates pointing to solid earnings before interest, taxes, depreciation, and amortisation (EBITDA) growth through the second half of 2026, while demand from yield buyers, particularly insurance companies and pension funds, continues to anchor valuations at tight levels.

The AI-driven capex cycle has become a defining feature of new issuance, with hyperscalers issuing roughly US$27 billion of AI-related high-yield supply financing data centre and infrastructure builds to date.8 Many of these deals benefit from robust structural protections including amortisation features, construction guarantees, and hyperscaler lease backstops. That said, we remain cautious on the sector given the execution risk inherent in such a rapid buildout.

Our preference remains for senior secured bonds backed by hard assets and contracted cash flows, including European debt secured on property and essential infrastructure, as well as select energy and defensive credits. These pockets may offer better downside protection and more reliable carry in an environment that demands a selective approach rather than broad beta exposure.

6. Source: Morgan Stanley US Credit Mid Year Outlook, 19 May 2026.

7. Source: Morgan Stanley US Credit Mid Year Outlook, 19 May 2026.

8. Source: Morgan Stanley US Credit Mid Year Outlook, 19 May 2026.

Strong EM fundamentals drove resilient performance over the last three months, despite a volatile geopolitical and oil market backdrop. We remain constructive on fundamentals, but rich valuations, renewed long risk positioning after April and May's rebound and oil price headwinds warrant caution. A Federal Reserve (Fed) shift toward rate hikes would compound pressure through higher rates, US dollar strength and spread widening.

Inventory drawdowns have cushioned shortages, but non-linear risks have risen – oil price spikes, second-round price impacts and demand destruction – as a result of the closure of the Strait of Hormuz. A gradual reopening will likely spur broad market rallies. EM local yields9 have repriced to reflect rising inflation risks (yields up 37 bps since the conflict started, -1.8% return), EM currencies (-1.7%) performed in line with local rates while EM hard currency sovereigns (+0.2% return, given spreads are 21 bps tighter) have outperformed. Tight spreads and limited duration gains mean returns will be largely carry-driven, with regional divergence likely to persist.

Sovereign spreads

With a gradual Strait of Hormuz reopening largely priced in, valuations are vulnerable to any delay, particularly for high yield oil importers. Technicals are mixed: fund flows have rebounded and primary market access is broadly open, but financing needs remain elevated, keeping supply high and risk allocations stretched. We maintain defensive views on the Gulf, Turkey and Egypt, while favouring Latin America for its oil-producer status and distance from the conflict. We see better entry points for weaker high yield credits emerging over coming months.

FX

We remain moderately constructive on EM currencies, supported by US/EM rate differentials, though extended speculative positioning and a potentially more hawkish Fed are key risks. In EM Asia, attractive valuations, trade surpluses and trade partner pressure for currency appreciation support a moderate FX recovery led by the Chinese yuan, Taiwanese dollar, Malaysian ringgit, South Korean won and Indonesian rupiah. The Indian rupee is the exception, pressured by current account deficits and inflation. In Latin America, risks are skewed to the downside amid growth concerns and political uncertainty: the Mexican peso is exposed to United States–Mexico–Canada Agreement headwinds and stretched valuations; the Colombian peso to twin deficits and political risk; and the Chilean peso to delays in Strait reopening. In EM Europe and Africa, we expect most currencies to track broader EM trends. The South African rand remains exposed to energy and metals dynamics, and we continue to avoid the Turkish lira amid growing glide path stresses.

Rates

We remain broadly neutral on EM rates. Hike pricing has moved significantly higher and the reopening of the Strait of Hormuz could quickly wrong-foot bearish positions. We favour curves that have already adjusted – Mexico, Brazil and Malaysia – over Asia low-yielders, where higher inflation, fiscal risks and central bank hikes point to further yield pressure.

9. As measured by the yield to maturity of the JPM GBI-EM GD, as of 29 May 2026.

The EM corporate credit landscape enters the second half on solid footing, with aggregate EM growth projected at 3.9%,10 declining inflation, and accommodative monetary policy supporting corporate fundamentals. EM corporates have delivered consistent earnings throughout 2025 and into 2026. Within the hard currency EM bond market, corporate bonds offer a broader opportunity set than sovereigns for diversifying risk, in our view, with BBB-rated credits offering attractive carry and roll-down potential. However, sovereign spreads sit uncomfortably tight by historical standards, US tariff policy remains a source of uncertainty, and the divergence between performing and stressed credits is widening.

Global high yield defaults are expected to remain benign at around 2% for 2026, well below the 4.5% long-term average.11 Yet the improvement masks increasing fragmentation, with CCC-rated borrowers and private credit portfolios bearing the brunt of stress. Bottom-up credit selection informed by company fundamentals will be the critical determinant of performance, in our view.

Latin America stands out to us as a particularly compelling pocket of value. The region presents a structurally under-levered corporate market: Latin American high-yield corporates carry average net leverage of around 2.8x versus 5.5x for US high yield, interest coverage of 5.4x versus 4.5x, and long-term hard-currency default rates less than two-thirds of global high yield. Despite this, spreads remain approximately 100-150 bps wider than US equivalents.12 This persistent, perception-based risk premium, driven by sovereign rating ceilings and the ‘zip code effect ’, whereby companies are penalised simply because of where they are located, keeps spreads elevated even when company fundamentals would support higher ratings. Utilities, metals and mining, and select consumer and industrial issuers offer the best relative value, with some US dollar-denominated names reaching more than 400 bps above Treasuries during Liberation Day volatility. Defaults in larger Brazilian credits, such as Braskem and Ambipar, appear idiosyncratic rather than precursors to broader distress.

The political and macro trajectory is arguably the most constructive in years. The region is undergoing a conservative shift bringing structural reforms, sustainable fiscal policy, and closer US trade ties. Mexico's post-2024 fiscal discipline is a powerful template for Brazil and Colombia ahead of their elections. Argentina has been transformative: inflation has fallen from triple digits to projected 16-20% in 2026, country risk spreads have narrowed to around 557-600 bps (their lowest since 2018) and the sovereign has returned to international markets near 6.5% coupons.13 Monetary policy is supportive, with rate cuts delivered in Brazil and Mexico during the first quarter, and Latin American industrials have potential to benefit from nearshoring-driven expansion in construction, logistics, and power infrastructure. The combination of resilient fundamentals, a closing fiscal credibility gap, and structural scarcity of institutional capital creates a compelling entry point, but dispersion is likely to be wide, and discipline in underwriting remains essential.

10. Source: Bloomberg, as of March 2026.

11. Source: JP Morgan, as of April 2026.

12. Source: JP Morgan, as of April 2026.

13. Source: Bloomberg, as of April 2026.

Asia credit enters the second half from a position of fundamental strength – and one that is well placed to navigate the risks outlined in the table above. Post-COVID deleveraging has strengthened IG metrics: the EBITDA/interest ratio has risen to 9.6x, net leverage sits at a healthy 1.1x, and the upgrade-to-downgrade ratio has recovered to 1.8x.14 In high yield, there were zero defaults in the first quarter, underscoring the market's clean slate. Defaults are forecast to decline to just 1.8% for the full year. This improved credit quality is precisely what provides resilience against the sovereign rating and macro pressures identified in the table above.

The Middle East conflict and Strait of Hormuz disruption have transmitted through energy channels. With roughly half of Asia's crude imports transiting the Strait, the shock has been material and explains the pressure vulnerable sovereigns have experienced. However, IG names, particularly the estimated 58% of the JP Morgan Asia Credit Index comprised of government-related entities, have been better cushioned, and EM Asia GDP growth remains the fastest globally at 4.7%.

Turning to the opportunity set, technicals directly underpin the carry thesis. First quarter net financing was around US$7 billion, Chinese onshore excess FX liquidity of US$557 billion continues flowing into offshore US dollar bonds,15 and second- and third-quarter maturities plus coupons provide a substantial reinvestment buffer. Order book coverage ratios above 7x in April confirm the strong unsated demand that supports a favourable technical backdrop.

On valuations, index spreads at 105 bps are optically tight, but all-in yields at 5.4% for duration of around four years validate the carry opportunity, in our view. Asia high yield trades 79 bps wider than US high yield rated BB,16 offering genuine value for comparable quality. Critically, the dispersion beneath tight headline spreads is a second key opportunity, in our view. From a country perspective, we believe Japan (corporate governance reforms outpacing what credit spreads reflect) and Hong Kong (sentiment-driven dislocations in financials and well-managed corporates) offer the most fertile ground. China and Indonesia require greater selectivity given compressed spreads and commodity sensitivity. Thematically, AI/tech enablers (semiconductors, batteries), defensive sectors (telcos, independent power producers) and subordinated paper (bank capital, corporate hybrids) stand out, while petrochemicals face headwinds from elevated crude and freight costs – a direct consequence of the Strait of Hormuz closure.

14. Source: JPMorgan, Asia Credit Outlook and Strategy 2Q26, April 2026. Data as of 31 March 2026.

15. Source: PBOC, JPMorgan, Asia Credit Outlook and Strategy 2Q26, April 2026.

16. Source: JPMorgan, Asia Credit Outlook and Strategy 2Q26, April 2026. Data as of 31 March 2026.

Global convertible bonds delivered strong asymmetric returns through the first half of 2026, continuing the structural resurgence the asset class witnessed in 2025. Through late May, the asset class captured more than 150% of equity market upside while limiting March drawdown participation to 80% – a convexity ratio of just under 1.9x. For investors benchmarked to the Global Focus Convertible Index, the equivalent figures are 80% upside capture and 56% downside participation.17

The reassertion of a higher-for-longer rate environment in the first half of the year – driven primarily by the Iran conflict and the resultant oil price shock – has proven a structural net positive for convertibles, even as it has created selective valuation headwinds for duration-sensitive names. Within the asset class, high-growth issuers have been increasingly concentrated in AI infrastructure, where corporates are riding the wave of hyperscaler capex commitments estimated at US$5 trillion over the next five years, spanning the full supply chain from semiconductor and memory suppliers through to alternative energy providers and data centre operators.

Crucially, much of the convertible issuance tied to this theme has been anchored by long-term contracts with strong IG corporates, providing visible and recurring cash flow streams. We think this lends the pipeline a more fundamental, less speculative character than might otherwise be expected in a high-growth thematic.

Year-to-date issuance volumes have reached approximately US$90 billion18 – more than double last year's run rate. The US has accounted for over half of total supply, with Asia contributing the bulk of the remainder. Given the strength of this pipeline, driven by significant capex requirements across sectors and corporate appetite to monetise elevated stock volatility, we expect full-year issuance to surpass last year's record US$167 billion.

We see the landscape for convertible bonds potentially remaining positive into the second half of 2026 as the structural tailwinds underpinning first-half performance – including strong issuance volumes and relative value versus both credit and equity – remain firmly in place. In a macro environment where the distribution of outcomes remains wide, the asymmetric payoff structure of convertibles is particularly well-suited, and we view any equity market weakness as an opportunity to add exposure at improved convexity levels.

17. Source: Bloomberg.

18. Source: Bank of America Merrill Lynch.

The climate and green bond market carries strong momentum into the second half of 2026. Corporate ESG bond issuance reached around US$120 billion through April, up approximately 19% year on year, led by Euro area issuers (+50% year on year). The US remains a softer spot, with sustainable-labelled bonds comprising less than 1% of US dollar IG issuance, down from 2.5% in 2024, as political headwinds weigh on supply.19 Barclays forecasts full-year global ESG bond issuance of around US$885 billion, broadly in line with 2025 levels. Investor appetite remains supportive: ESG fixed income funds attracted approximately US$4 billion of net inflows in the first quarter,20 with pronounced outperformance in global, Asian, and EM categories.

Several structural themes underpin the constructive outlook. First, energy grid and utility capex is accelerating – global grid investment reached around US$490 billion in 2025, growing at a 4% compound annual growth rate (CAGR), with smart grid and energy storage segments growing at a CAGR of 9% and 20%, respectively.21 European utilities are a key conduit: 61% of year-to-date utility bond issuance is sustainability-themed, backed by transformative capex plans from National Grid (£100 billion), Enel (€84 billion), and Iberdrola (€58 billion).

Second, Asia-Pacific is emerging as a critical growth engine, accounting for around 50% of the world's US$2.1 trillion energy transition investment. Asia ex-China ESG bond issuance rose 37% year on year, with green bonds comprising two-thirds of regional supply.22 India, Korea, the Philippines and Thailand are all posting strong growth, supported by ambitious renewable targets.

Third, AI and data centre expansion is creating significant financing opportunities – European data centre power demand is forecast to more than double to 89 terawatt-hour (TWh) by 2030, driving demand for green-labelled infrastructure financing.

Fourth, the Iran conflict and Strait of Hormuz disruption – affecting roughly a fifth of global oil and liquefied natural gas supply – has reinforced the strategic imperative for domestically sourced clean energy, with Brent surging above US$100 per barrel.

On the regulatory front, the SFDR 2.0 reform introduces a new Article 7 "Transition" category alongside stricter definitions for sustainable products, while the likely adoption of the EU 2040 climate target (90% greenhouse gas reduction) provides long-term policy predictability. In Asia, 13 sustainable finance taxonomies are now in effect with two more upcoming, and countries introducing new frameworks have consistently seen a pick-up in labelled issuance momentum.

19. Source: Barclays, Asia Commitment Checks — Energy Transition at the Crossroads, 12 May 2026.

20. Source: Barclays, QPS ESG Quarterly Credit Update Q1 2026, 28 April 2026.

21. Source: JPMorgan, The Sustainable Investor - Make the Grid Great Again, 9 March 2026.

22. Source: JPMorgan, Sustainable Investing 2026 Outlook, 1 December 2025.

New catastrophe (cat) bond issuance has been active year to date, with around 57 new deals announced and US$13.7 billion of notional priced, bringing the size of the space to around US$64 billion.23 We have seen plenty of (US wind and quake) peak peril deals as well as US wildfire; cloud outage; UK terrorism; Kyrgyz Republic / Tajikistan quake; and other non-peak perils. Peak peril spreads remain adequate. However, non-peak perils, in addition to making a portfolio less dependent upon Atlantic activity, often carry a modelling uncertainty premium and offer attractive spreads relative to their expected loss.

Forecasters are suggesting that we may be headed for a strong or very strong El Niño (where Pacific Ocean temperatures are above their long-term average).24 The impact is global (ranging from fishing stock migrations to wildfire) but insofar as cat bonds are concerned:

- Warmer sea surface temperatures in the Pacific are conducive to storm formation there

- Increased wind shear suppresses strengthening of storms in the Atlantic

- A wetter winter may suppress California wildfire in the near term, but the longer-term picture is more mixed as the fuel load increases

- Earthquakes are unaffected

It will come as no surprise, therefore, that seasonal forecasts for the Atlantic are a little lower this year. We would caution that this comes with several caveats. Firstly, as we demonstrated in an article earlier this year, the accuracy of seasonal forecasts differs little from a simple rolling average. Secondly, to cause large economic damage, a storm needs to have strengthened prior to landfall, and to do so in an area of high insured value.

One bad storm is all it takes.

23. Source: Man Group database, as of 31 May 2026.

24. Source: https://www.bbc.co.uk/weather/articles/cvgzn11v421o.

The ICE BofA Global High Yield Index OAS sat at 284 bps as of the end of May 2026. This divergence between price and underlying fundamental reality is a key watchpoint. It also offers a rich source of opportunity for active managers able to distinguish between credits that warrant tight spreads and those that do not. A potential outcome in the second half is moderate widening and greater dispersion, creating precisely the environment in which bottom-up security selection tends to outperform.

AI disruption and geopolitical risk have dominated the first half and are expected to remain defining forces into the second half. The rapid advancement of AI capabilities has reshaped market expectations, with investors increasingly questioning the durability of business models across software and services sectors. The risk for AI in credit is not just as a theme but as a leverage event — capex estimates for the five largest US technology companies have risen sharply to roughly US$800 billion this year and US$1.2 trillion in 2027,25 materially increasing the debt load of a concentrated group of issuers. AI-related exposure is becoming pervasive across portfolios and apparent diversification across issuers and sectors risks reflecting a single macro bet, elevating correlation risk that active security selection is well-positioned to navigate.

On geopolitics, the escalation in the Middle East in late February effectively closed the Strait of Hormuz, sending Brent crude skyrocketing from approximately US$70 to over US$105 per barrel26 in less than three weeks, with knock-on implications for supply chains, inflation and the rates path. Any resumption of the conflict could sustain elevated oil prices and create further inflationary pressure, complicating Fed policy.

The refinancing wall looming in 2026/2027 adds further texture to the opportunity set. Companies that issued debt during the ultra-low-rate era and now face punitive rollover costs are increasingly visible in our models, as are the growing tally of companies where interest costs exceed income.

25. Source: Morgan Stanley Mid Year Outlook.

26. Source: Bloomberg.

After a strong 2025, when securitised credit indices returned 6.5%-9.5%, spreads remained resilient but tight in the first half of 2026, limiting broad-based beta return potential for the second half. We see better opportunities in sub-sector and security selection, supported by active implementation. In agency mortgage-backed securities (MBS), which are backed by US government credit, we favour prepayment-protected specified pools over generic cheapest-to-deliver to-be-announced (TBA) collateral, where convexity costs have nearly doubled in recent years and remain elevated. Put simply, generic TBA-like collateral has become more rate-sensitive and is likely to underperform during periods of rate volatility.

In credit, we are constructive on CLOs, as spreads remain toward the wider end of recent ranges, though private-credit headlines and a higher-for-longer rate backdrop may drive episodic volatility. On the CLO collateral side, exposure to software-sector loans warrants scrutiny. We expect the CLO credit curve to steepen from AAA to B tranches, with collateral quality and manager selection increasingly important in lower-rated tranches. We also expect dispersion across commercial mortgage-backed securities (CMBS) and asset-backed securities (ABS), including in hotel CMBS and shipping-related ABS, given potential exposure to fuel-cost and availability shocks amid Middle East tensions. With spread income likely weaker than in 2025 and dispersion driven by subsector, collateral and structure, active systematic management and portfolio optimisation should be well positioned to capture timing- and quality-driven alpha.

Figure 6. Structured credit: spread monitor

Source: JP Morgan, as of 29 May 2026.

Private markets

We expect middle market direct lending to continue to be an important source of yield and diversification in the second half of 2026, particularly in a potentially higher-for-longer rate environment. Quality middle market lending, particularly sponsored deals with robust covenant packages, continues to offer attractive yield pick-up relative to the broadly syndicated loan market, in our view. This would become more significant if merger and acquisition (M&A) volumes remain subdued, as the upper end of the market has historically been more susceptible to competition-driven yield compression than the core middle market.

Items to watch:

- Fundraising versus opportunity set: Managers that raised significant funds in recent years have found it challenging to match historical deployment rates in a suppressed M&A environment. This mismatch can potentially result in adverse credit selection risk. We believe that managers that were more prudent in matching capital raises with an actionable opportunity set, without compromising on credit selection, are likely to be better positioned to navigate any potential economic softness

- Credit fundamentals: Much of the recent negative commentary reflects a view that the industry loosened standards during its period of rapid growth. This is a broad generalisation and each manager warrants individual assessment. Exposure to software and technology illustrates the point: while industry-level exposure runs at roughly 20%, some managers exceed 30% while others sit below 10%. Given the uncertainty around AI's effect on the sector, diversification remains a core discipline

- Capital base and fund structure: The retail and wealth channels have grown rapidly, representing a meaningful tailwind for managers over the past five to seven years. That tide has turned, at least for now, placing pressure on general partners, managing vehicles with quarterly redemption features. Managers with more institutional capital bases and funds without such features are likely to be better placed to focus on portfolio construction and management

Key risks and how to manage them:

- Credit cycle and issuer stress: Underlying borrower fundamentals have not seen material deterioration to date, but that could change in the current volatile macro environment. We think it’s prudent to stress-test portfolios across rate and revenue shocks and avoid overconcentration

- Competition and strategy crowding: Fee compression and looser underwriting can erode returns and create significant name overlap across managers. Transparency is important to ensure true diversification across general partners

- Operational and structural risks: Collateral valuation, covenant enforcement and documentation quality all matter. Structures designed to offer liquidity in an illiquid asset class have the potential to force managers to take unnatural action when that liquidity is requested

We may finally start to see dispersion in returns in direct lending. Managers with disciplined origination, strong workout capability, transparent valuations and sector knowledge should differentiate in a positive way in the coming year(s).

The first half of 2026 was defined by geopolitical shock and perceived stress in private credit markets.

Credit quality in pockets of private credit continues to deteriorate. The industry default rate has risen to 5.8%,27 and forecasts suggest it could reach 8% over the next year.28 BDCs are trading at a roughly 22% discount to net asset value (NAV),29 which is a level not seen since the COVID-19 pandemic. Bad PIK, a proxy for hidden distress, has climbed to 6.4% of borrowers, up from 2.5% at the end of 2021.30 Meanwhile, retail redemptions have accelerated sharply, with approximately US$21 billion in withdrawal requests in the first quarter alone.31 Some major platforms have gated or capped redemptions, meeting only about half of requests. This self-reinforcing cycle of outflows, share price declines, and negative sentiment is pressuring the broader credit ecosystem.

AI disruption is compounding these pressures. The industry carries approximately 26% exposure to software and technology, and over US$330 billion of software and tech debt matures through 2028.32 Refinancing is becoming significantly more difficult as lenders reassess the durability of SaaS business models in an AI-driven world.

For opportunistic credit managers, this environment is becoming increasingly attractive. Managers that have avoided software and technology concentration, declined to underwrite loans on an annual recurring revenue (ARR) basis, and stayed away from unprofitable companies are likely to be better positioned to navigate the current stress. The most presciently positioned strategies have focused on super-senior positions at low loan-to-values, defensive assets with hard collateral, and sectors such as power, energy infrastructure, and specialty finance that benefit from structural tailwinds.

In private markets, stress among direct lenders is creating opportunities to provide capital on favourable terms. In public markets, if spreads widen materially, our flexible mandate allows us to pivot quickly toward tradeable opportunities in high-yield bonds and leveraged loans.

We do not believe private credit poses a systemic risk as it represents roughly 6% of US gross domestic product (GDP)33 with minimal leverage and institutional loss-bearing. However, we do believe the asset class is undergoing a meaningful repricing of risk. For selective, well-structured credit investing, the second half of 2026 should offer fertile ground.

27. See: https://www.fundssociety.com/en/news/alternatives/u-s-private-credit-de…. As of January 2026.

28. See: https://www.cnbc.com/2026/03/25/private-credit-defaults-loan-quality-de…. As of March 25, 2026.

29. Source: https://www.bdcs.com/#contactForm. As of April 1, 2026.

30. Source: Lincoln International. https://www.lincolninternational.com/news/the-lincoln-private-market-in…. As of February 11, 2026.

31. See: https://www.privateequitywire.co.uk/private-credit-fund-redemption-requ…. As of Q1 2026.

32. See: https://www.gurufocus.com/news/8785323/private-credit-sector-faces-chal…. As of 9 April 2026.

33. Source: Bloomberg, Preqin, as of Q3 2025.

The credit risk sharing market enters the second half of 2026 with powerful momentum, underpinned by record issuance, a deepening investor base, and a regulatory environment that is finally catching up with the asset class's maturity. Banks issued US$41 billion of significant risk transfer (SRT) transactions globally in 2025, up from US$29 billion the prior year. 2026 is on track for more than 20% further growth with no sign of deal delays from geopolitical disruption.34

Europe remains the largest and most mature market, while the US continues to gain traction as regulatory clarity improves and participation widens, including regional lenders managing concentrated commercial real estate (CRE) exposures. The bank balance sheet securitisation market has grown significantly over the past five years and looks set to continue, driven by clearer regulation, wider bank adoption of the technology, and strong incentives to free up risk-weighted assets rather than raise equity capital.

The regulatory tailwinds are substantial and accelerating. The EU securitisation package proposes targeted amendments to the Capital Requirements Regulation (CRR) designed to promote SRT market growth, including replacing the existing mechanical test with a more flexible principle-based approach and harmonising supervisory assessments.

Since January 2026, the European Central Bank (ECB) has been operating an SRT fast-track approval process, cutting its response times from three months to just eight working days. The European Parliament finalised its proposed amendments to the Securitisation Regulation and CRR in early May 2026, with trilogue negotiations expected in the second half of the year. While the full benefits of these reforms will take time to materialise, the direction of travel is unambiguously supportive, and new economic priorities around digitalisation, climate transition, and European defence spending may further incentivise banks to expand their use of SRTs.

The credit backdrop, meanwhile, is constructive but demands selectivity. European bank profitability remains robust, with asset quality and capital buffers solid, and while a moderate pick-up in default rates is expected, capital headroom will comfortably cushion the downside. This means the originating banks behind CRS transactions remain strong counterparties with well-provisioned balance sheets. However, dispersion is widening as corporate credit is displaying late-cycle characteristics, and the bifurcation between performing and stressed credits is becoming more pronounced. In this environment, experienced managers capable of rigorous due diligence and selective underwriting across diverse loan portfolios will be the true differentiators, as not all SRTs are created equal and growth detached from fundamentals can undermine the stability these structures are designed to support.

34. Source: With Intelligence, as of April 2026.

We maintain a constructive view on US residential debt heading into the second half. The core drivers underpinning our thesis for the first half remain intact: a structural housing supply deficit, an aging housing stock, and sustained rental demand from households unable to access homeownership at current price and rate levels. Home price appreciation has decelerated but remains positive. Case-Shiller printed +0.7% year-on-year in March, the most recent available data.

We expect transaction volumes to remain muted through 2026 and into 2027, broadly consistent with 2025 levels. Days on market remain below historical norms. The "lock-in" effect – whereby existing homeowners on low fixed-rate mortgages are disincentivised to transact – continues to suppress resale supply, maintaining pressure on inventory. Mortgage rates remain range bound. The 30-year fixed rate mortgage is currently averaging 6.3–6.5%, having briefly dipped below 6% in February before geopolitical-driven inflation concerns pushed rates higher.

Regional divergence continues to sharpen. Sunbelt and West Coast markets face elevated supply and rising insurance costs. However, early signs of stabilisation are visible in Florida and Texas, suggesting these markets may be past the trough. The Northeast and Midwest present a different picture, where limited new construction has kept inventory tight, and home prices are rising faster. Credit selection remains critical given this disparity.

Multifamily fundamentals are showing improvement. The peak of the construction delivery cycle now appears largely behind us. As new deliveries taper over the next two to three years, fundamentals are expected to revert toward positive rent growth and gradual recovery of occupancy. Construction loans with completions over the next two to three years are well-positioned relative to this anticipated inflection point.

The structural housing shortage shows no near-term resolution. Affordability constraints – high prices, elevated mortgage rates, and the lock-in effect – continue to suppress homeownership rates and sustain rental demand across both single-family and multifamily segments. On the supply side, immigration policy shifts and an aging workforce are tightening labour costs and availability, while persistent materials cost inflation, compounded by tariff exposure, is bearing down on construction economics. Renovation and remodelling remain a durable theme given the aging housing stock (an estimated 45-year median age of owner-occupied homes), though baseline construction cost escalation is expected with potential for higher increases in tariff-sensitive or labour-intensive trades.

Housing policy developments warrant monitoring. The 21st Century ROAD to Housing Act, a bipartisan bill combining House and Senate housing legislation, includes provisions restricting institutional investors from purchasing single-family homes above a defined threshold (350 homes). The Senate and House passed differing versions, with one key point of contention centring on the treatment of build-to-rent developments. This is an area we are closely monitoring.

Credit quality indicators remain supportive. Only 2.2% of mortgaged properties have negative equity, serious delinquency rates are low, and real estate equity and stock market holdings are at historical highs.

Our preference within US residential debt is for short duration, small balance credits and multifamily developments in supply-constrained markets.

You are now leaving Man Group’s website

You are leaving Man Group’s website and entering a third-party website that is not controlled, maintained, or monitored by Man Group. Man Group is not responsible for the content or availability of the third-party website. By leaving Man Group’s website, you will be subject to the third-party website’s terms, policies and/or notices, including those related to privacy and security, as applicable.