Quote of the Week:

"I have a reputation ... of speaking the truth at all times and not sugar- coating things. And that may be one of the reasons why I haven’t been on television very much lately."

Is the S&P500 Index Useful Anymore?

The S&P500 Index has recovered from the nadir of the coronacrisis: it is now down only 6% from its pre-crisis peak. However, the headline figure slightly obscures the reality of the new market we find ourselves in.

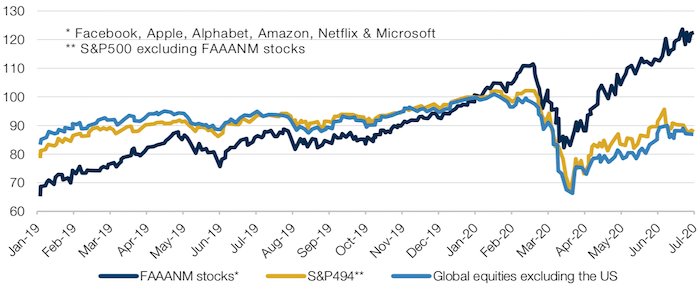

The outperformance of the technology (read Growth) stocks that we saw before the coronacrisis has continued apace in its aftermath. Research from Minack Advisors shows that the six biggest tech names – Facebook, Apple, Alphabet, Amazon, Netflix and Microsoft – are actually trading at a premium compared to before the crisis. By contrast, the remainder of the S&P500 Index is still below its pre-crisis highs, a position matched by other global equities.

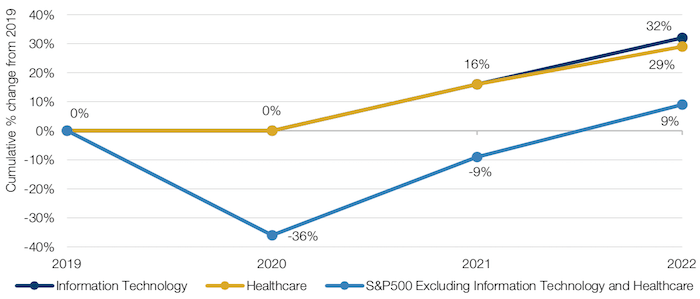

This outperformance makes sense. Analysis by BCA Research shows that EPS growth estimates in technology and healthcare stocks – whose operating models have either been unaffected or enhanced by the coronavirus – are flat for 2020 and 16% for 2021 (Figure 2). The rest of the index, more reliant on physical sales and the ability of customers, employees and goods to move unimpeded, has EPS growth estimates of -36% for 2020 and -9% for 2021.

In effect, we now have two equity markets: a small group of stocks large enough to drive index level data on their own, and a multitude of smaller stocks still battered by coronavirus headwinds. This begs the question: is this bifurcation killing the S&P500 as a useful depiction of the US equity market?

Figure 1. Six Biggest Tech Names Versus the Rest of the S&P500 Index

Source: Minack Advisors; as of 7 July 2020.

Rebased to 100 as of 1 January 2020.

Figure 2. EPS Estimates for Information Technology, Healthcare and the Remainder of the S&P500 Index

Source: BCA Research, Refinitiv, IBES; as of 7 July 2020.

The Future Isn’t What It Used to Be

How might the coronacrisis affect long-term returns in equities and bonds?

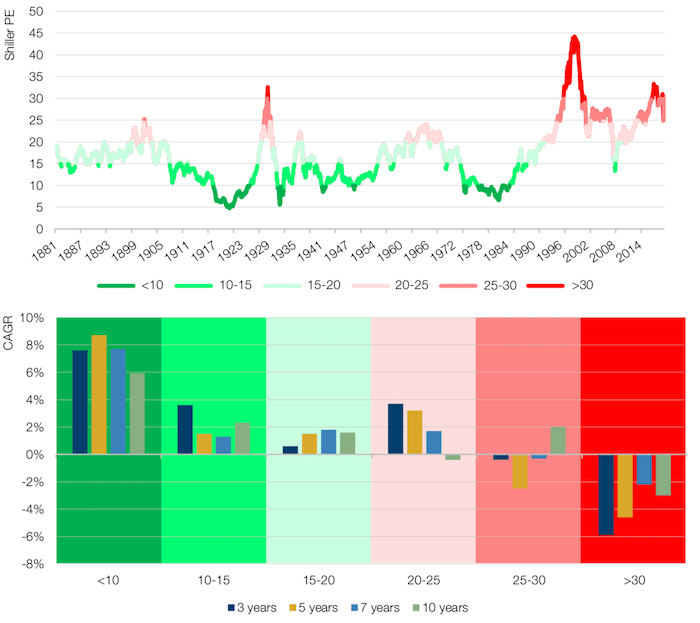

We’ve previously written on the relationship between US equity returns and the Shiller cyclically adjusted price to earnings ratio (‘Shiller CAPE’). Put simply, the higher the Shiller CAPE, the worse the compound annual growth rate (‘CAGR’) for US equities over a 3-, 5-,7- and 10-year horizon (Figure 3).

March 2020 saw the Shiller CAPE fall six points, from just under 31 to just under 25. This was the second-largest monthly fall on record, beaten only by the 8-point fall in November 1929 – which just happened to herald the start of the Great Depression. The subsequent risk rally in April drove the Shiller CAPE back to 26, and it has since risen to almost 30 as of June.

So, the Shiller CAPE predicts that the outlook for equities is not pretty: a ratio between 25 and 30 has historically implied negative equity growth rates over the subsequent seven years, whilst a ratio more than 30 has implied a negative CAGR across all four timeframes.

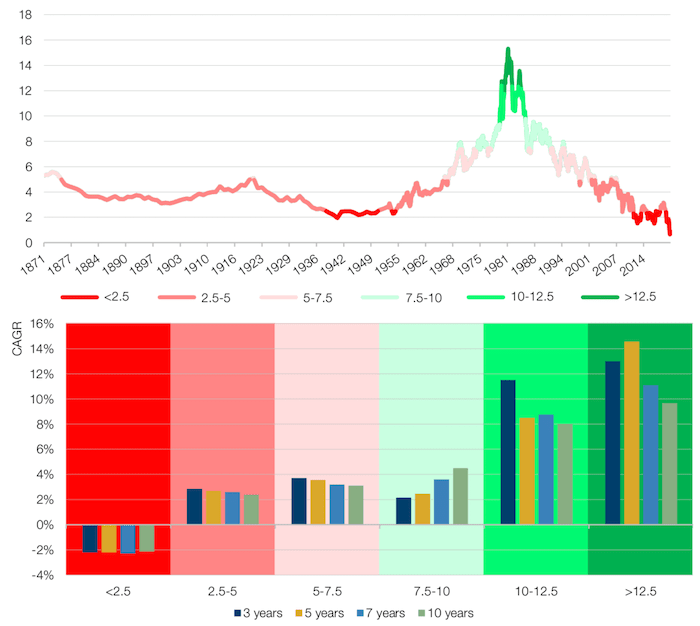

The picture is even more stark for US Treasuries. Figure 4 shows yield for 10-year US Treasuries, and the subsequent CAGR. We are now deep into unprecedented territory, at the end of the longest bond bull market in our dataset, with an implied negative CAGR across all four-time horizons.

When taking into consideration the construction of the traditional 60-40 portfolio, these implied negative growth rates for both equities and bonds are likely to pose a real challenge for managers over the coming decade. Quite simply, this is the only time in the dataset where the outlook for both asset classes was simultaneously so poor – and that includes the Great Depression.

Figure 3. US Shiller CAPE

Source: Robert Shiller, Bloomberg, Man Solutions; as of 9 June 2020.

Figure 4. 10-year US Treasury Yields

Source: Robert Shiller, Bloomberg, Man Solutions; as of 9 June 2020.

With contribution from: Pierre-Henri Flamand (Man GLG, CIO Emeritus and Senior Investment Advisor, Man GLG) and Teun Draaisma (Portfolio Manager, Man Solutions).

You are now leaving Man Group’s website

You are leaving Man Group’s website and entering a third-party website that is not controlled, maintained, or monitored by Man Group. Man Group is not responsible for the content or availability of the third-party website. By leaving Man Group’s website, you will be subject to the third-party website’s terms, policies and/or notices, including those related to privacy and security, as applicable.