Introduction

When we started as research associates at Morgan Stanley in the mid-1990s, we were trained to think along multiple time horizons. Well, two time horizons, to be precise. For portfolio allocations at time t, we needed a view of the market environment from t=0 to t+6 months. But, so as not to get lost in the hurly-burly of the here and now, we were also taught to try and understand longer-term regimes – say years t+1 to t+5, or beyond. Or as one of our mentors, Barton Biggs, used to say, we had to distinguish between the cyclical and the secular.

Our cyclical view today is one of a slowing US economy, coupled with an enduring inflation overshoot and therefore a relentlessly tightening Federal Reserve. Our secular view is one of a new higher and more volatile inflation regime (see, for example, Inflation Regime Roadmap and The Best Strategies for Inflationary Times).

What we want to do in this article is to introduce our first thoughts about a second, related secular theme that we believe could be investable for the next five years and which is only just getting going – to wit, a new capex supercycle.

In this article, we will look at the background of G7 capital investment, which has languished; then examine the reasons why it might now pick up. Finally, we will suggest what impacts a secular investment boom might have on G7 asset markets.

G7 Secular Stagnation…

In his widely noted 2014 speech resuscitating Alvin Hansen’s concept of “secular stagnation”, Larry Summers set out the three factors that he believed had contributed to what he identified as a new bout of economic torpor.1 These included falling hours worked and falling total factor productivity, but by far, the biggest catalyst was low capital investment. So, assuming Summers was right, it follows that stimulating capital investment could prove an outsized stimulant to boot-strap western economies out of their malaise.

…Driven by an Asian Investment Boom…

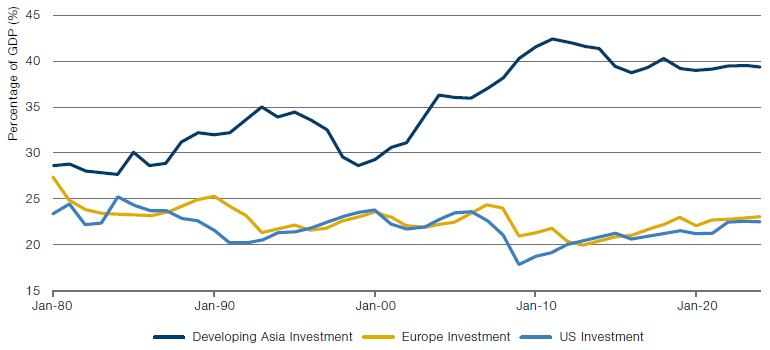

The last 20 years have seen an investment boom in Asian economies, accelerated by China’s 2001 accession to the World Trade Organisation. The corollary has been the secular decline in fixed capital formation in G7 economies, which outsourced production and jobs to Asia. Figure 1 illustrates the extent of this divergence. Since 2001, developing Asia’s capital expenditure rose from 30% of GDP to 40% of GDP, while that in the US declined from 22% to just over 20% before recovering around the pandemic. Europe has followed a similar path.

Figure 1. Regional Investment as % of GDP

Source: Minack Advisors; as of 31 March 2022.

This process was both ‘A Good Thing and A Bad Thing’, as Yeatman and Sellar would say.2 For Asian workers, and for Asian economies generally, it was an unmitigated Good Thing. On a purchasing power parity (‘PPP’) basis, developing Asia’s GDP per capita rose at a nearly 8% annual rate for the 20 years after 2001. In absolute terms, it rocketed from USD3,000 to nearly USD13,0003 and lifted hundreds of millions out of poverty. Western consumers also enjoyed the process, with imported goods prices from China, for example, unchanged over 20 years.4 Cheap Chinese manufactured goods poured into western markets, prompting large Chinese current account surpluses which were recycled via the capital account into a huge net international investment surplus (now reaching USD2 trillion).5

…At the Expense of Western Workers…

But there was one big loser – the western worker – whose job was exported to Asia.

And along with the job went investment in productive capacity, prompting the long stagnation of western capital spending, which brought with it Summers’ secular stagnation. Western workers now had to compete ferociously for their jobs, and compete on price. Wages were nailed to the floor. Western corporations benefited hugely from a secular decline in the wage share of GDP as the profit share went to 100-year highs – they’d not seen anything like this since the 1920s. Not only were corporate margins at century-long highs, but capex was very low given the lack of investment, so return on invested capital and free cash flow generation was off the charts. Without wage or goods inflation, there was no inflation full stop. So central banks could keep interest rates very low.

In the 15 years from 1999 to 2014, US household median real income actually fell by 13% – in a world where aggregate net wealth was rising at an annual rate of 6%.

It was the perfect cocktail for corporate profit and valuation. Net worth of the US consumer rose exponentially, from USD40 trillion in 2000 to USD150 trillion today – and that’s despite the deflation of the TMT bubble in 2000-03, the GFC of 2008, the Eurozone crisis of 2010-11 and the global pandemic of 2020-21 – basically, western consumers in aggregate kept getting richer whatever you threw at them.

The problem, though, was that this wealth was very unevenly distributed.6 Why, then, wasn’t there a revolution? Well, if you couldn’t earn it, you could borrow it. Debt was extended to the lower half of the income distribution largely via the housing channel. Cue the financial crisis of 2008.7

To work off the debt, austerity was introduced across many western economies, squeezing the real incomes of workers even further. In the 15 years from 1999 to 2014, US household median real income actually fell by 13% – in a world where aggregate net wealth was rising at an annual rate of 6%8 – prompting Larry Summers to write his famous paper.

…Changing Political Priorities

Which brings us to today.

Workers have woken up to their plight and are demanding change. Politicians, obtuse as they may sometimes appear, are always keen to be re-elected and have responded with aspirations to “level up”9 and “build back better”.10 Even China has taken note, with its policy on Common Prosperity which is intended to spread the wealth. So, whether for cyclical or (more likely, we think) secular reasons, wages in G7 economies are starting to inflate. The way we see it, it is inevitable that wages for the lower half of the income distribution will have to rise in real terms in order to restore any concept of fairness in society. This will have to be not a one-off level re-set, but a multi-year process.

Higher wages require better jobs, or they’ll be economically unsustainable. How do you get better jobs? By investing in productive capacity “at home”. UK Chancellor of the Exchequer Rishi Sunak summed this up in March, with a warning that “unless productivity and growth increase, people will begin to lose faith in the moral and material case for free markets. The problem is no longer the government – businesses simply aren’t investing enough”. He also added that his priority was “to cut taxes on business investment in the years ahead”.11

So, that’s a rather long-winded – but necessary – summary of the background to the coming G7 capex boom, which hopefully establishes the need for increased capital investment. But what are the actual drivers that can set it in train?

Drivers of the Capex Boom

Until a month ago, there were four main drivers of a likely capex boom that we have been thinking about for a couple of years now – see Inflation Regime Roadmap, for example. These are:

- Corporate sector substitution of capital for labour as the wage share in GDP rises, as discussed above;

- Net zero and the drive for renewable energy;

- Supply chain independence as countries secure their access to essential components and materials, independent of global supply chains;

- “Build back better” style policies to refresh public infrastructure and

“level up”;

And now that Russia has fired the starting rockets on Cold War III (Professor Niall Ferguson’s phrase), there is a very obvious fifth driver… - …Defence spending.

If It Happens, What Does It Mean?

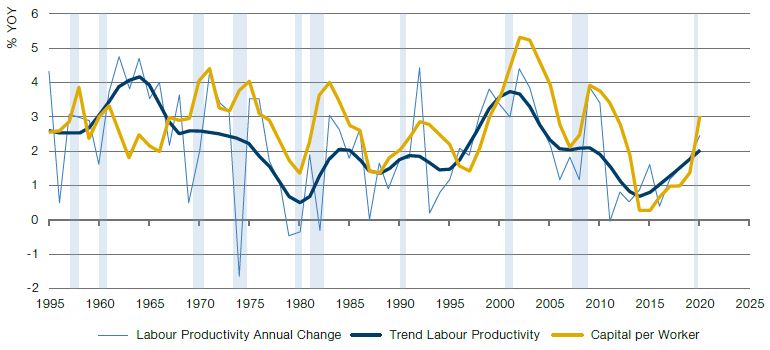

There are not many relationships in economics that seem as clear to us as that between capital spending and productivity. We say this as non-economists, of course! Our friend and former colleague Gerard Minack – as serious an economist as you’ll find – produced Figure 2 which tracks the relationship. He also provided the list of capex drivers that we just cited.

Figure 2. US Labour Productivity and Capital Deepening

Source: Minack Advisors; as of 31 March 2022.

Note: Capital per worker is 5-year average growth in capital per hour worked.

The chart shows three very interesting things. First, that capital spend per hour worked hit 60-year lows in the 2010s. Second, that labour productivity promptly did the same. But third, that the pandemic has seen capital spending start to recover very smartly, bringing productivity with it. If Gerard is right, and we think he is, then this could be the start of long capex wave that could promote a productivity boom.

Investment Implications

Our initial thoughts are that the following are some of the most interesting areas:

- Semiconductor capital equipment;

- Capital goods;

- Engineering;

- Construction;

- Robotics;

- Sensors;

- Visualisation software and hardware;

- Raw materials;

- Transport and shipping;

- Uranium and nuclear power generation;

- Other renewable electricity generation enablers.

Bringing investment back “home” should mean a reversal of the globalisation process and the de-coupling of economic cycles to some degree. So, country investing could make a comeback.

At the macro level, we face a tension between higher and more volatile inflation – promoting shorter cycles with larger amplitude than we have been used to, on the one hand, and potentially structurally higher productivity growth on the other. This could mean that corporate profit can hold up reasonably well for companies with large investment opportunities, but will be punished for companies without those opportunities in the new world. As such, there could be good dispersion of returns within equity indices – fertile territory for alpha creation, one would hope.

At a country level, bringing investment back “home” should mean a reversal of the globalisation process and the de-coupling of economic cycles to some degree, meaning that regional – and even national markets – might offer very different returns at a given starting point. So, country investing could make a comeback.

At the very least, we believe that secular stagnation is dead and we are entering a period of higher nominal GDP growth but shorter and more violent cycles. The days of buy-and-hold are now, in our view, behind us.

1. See Secular Stagnation, Hysteresis, and the Zero Lower Bound, NABE, June 2014.

2. See 1066 And All That, RJ Yeatman and WC Sellar.

3. Source: World Bank

4. Source: BLS

5. Source: IMF

6. See Capital in the Twenty-First Century, Thomas Piketty, for details.

7. See our article Debt is Capitalism’s Dirty Little Secret, Financial Times, July 2009.

8. Source: Bureau of Economic Analysis.

9. https://www.theguardian.com/politics/2021/aug/15/levelling-up-what-is-it-and-what-has-boris-johnson-proposed

10. https://www.whitehouse.gov/build-back-better/

11. https://www.ft.com/content/cd7e7110-7507-4047-8513-f51ff1f8ace6

You are now leaving Man Group’s website

You are leaving Man Group’s website and entering a third-party website that is not controlled, maintained, or monitored by Man Group. Man Group is not responsible for the content or availability of the third-party website. By leaving Man Group’s website, you will be subject to the third-party website’s terms, policies and/or notices, including those related to privacy and security, as applicable.