Introduction

The biggest economic challenge for policymakers today seems abundantly clear – free developed economies from the shackles of secular stagnation, raise inflation expectations (within reason) and restore the dynamism of the post-war period. In assessing this, we find it interesting looking at history to see how a similar challenge was overcome in the past. We are not looking for a precise recipe here: no historical analogue is ever perfect, but the 1930s does contain striking parallels with the economic situation in which we now find ourselves.

To this end, we recently read Robert Dallek’s acclaimed single volume biography of the architect of America’s salvation from the Depression. In Franklin D. Roosevelt – A Political Life (Penguin, 2018), we find a blow-by-blow account of what it took to raise a great nation from its despair, in terms both of his economic policy and his personal and political outlook. It is remarkable how many of today’s politicians seek to embrace Roosevelt’s legacy, from President Joe Biden’s comment that the Covid-crisis “may eclipse what FDR faced” (quoted in the Guardian, 22 May 2020), and his recent visit to Warm Springs, Georgia, where FDR recuperated from polio; to Alexandria Ocasio-Cortez’s Green New Deal; to Boris Johnson’s levelling up agenda.

What follows is not a book review, rather our notes of what seemed to be the most important elements of the Roosevelt reflation as relayed by Dallek. We divide them into observations of economic policy, first, and of the personality traits of FDR the man, second. Quotations are direct from Roosevelt’s speeches and letters, as quoted by Dallek, unless marked (Dallek), in which case they quote the text of the book itself.

Economic Policy

We can arbitrarily think about FDR’s economic policy response in six broad categories, some more crucial than others, but all of which played their part in the recovery. Here, we list those categories and fill in some of the more important actions undertaken:

- Inflate, not deflate

- “It is simply inevitable that we must inflate and though my banker friends may be horrified, I still am seeking an inflation which will not be wholly based on additional government debt”.

- Secure the banks

- Declares bank holiday 9 March 1933 as prelude to new banking bill – backstops the banks, but doesn’t nationalise them;

- After the first fire-side chat on 12 March 1933 when banks re-opened the following Monday, people queued to put their mattress money back on deposit;

- June 1933: signs the Banking Act to regulate Wall Street, containing the Glass-Steagall laws separating commercial and investment banking, and creating the Federal Deposit Insurance Corporation (‘FDIC’), which guaranteed deposits up to USD5,000 (99% of all deposits being covered).

- Apply monetary stimulus

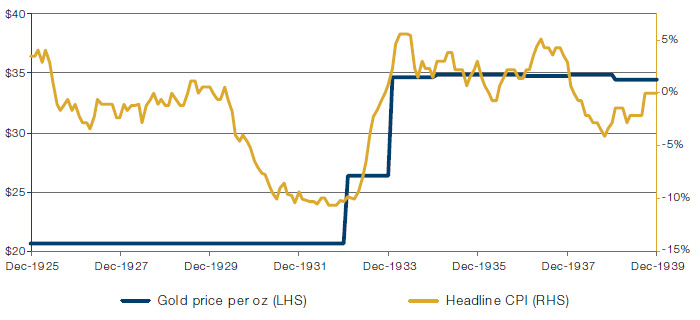

- April 1933: took the dollar off the gold standard by signing up to the Thomas Amendment for cheaper US dollars – which his own budget director, Lewis Douglas, declared “the end of Western civilization”; embargoes dollar exports and outlaws the private ownership of gold. Dollar value of gold rises from USD27 to USD35 – a 30% dollar devaluation;

- July 1933: FDR refuses to verbally back the external value of the US dollar at the London Conference of Nations;

- January 1934: FDR signs Gold Reserve Act that fixes the dollar 41% below prior gold parity.

- Apply fiscal stimulus / put people to work

- Legalized 3.2% proof beer and light wine – ending Prohibition, getting people to go out again;

- March 1933: creates the Civilian Conservation Corps (‘CCC’) to put 250,000 young people between ages 18-25 to work immediately so they did not become used to being on the dole. They earned USD1 a day (very low wage), but were required to send the bulk of the wage home to their families. “Over the next nine years, 3 million young people would cycle through the CCC, planting three billion trees, creating 800 state parks, stocking one billion fish in the streams and lakes, containing scores of forest fires” (Dallek p148, paraphrased);

- April 1933: Agricultural Adjustment Act (‘AAA’) aimed to raise farm prices and income by paying farmers for reduced production – farmers were 30% of the labour force;

- April 1933: appropriated USD500 million for state budget relief via the Federal Emergency Relief Administration (‘FERA’), which was the successor to the TERA of 1931;

- May 1933: creates the Tennessee Valley Authority (‘TVA’) to construct dams on the Tennessee River to avoid seasonal flooding and associated topsoil erosion that had decimated farmers’ livelihoods; and to provide electricity to the 90% of farms that lacked it in the seven southern states covered;

- November 1933: creates the Civil Works Administration (‘CWA’), employs four million people in manual labour rebuilding the country’s infrastructure;

- August 1934: FDR’s budget director Lewis Douglas resigns in protest at his unbalanced budgets.

- Raise real incomes

- May 1933: signs the National Industrial Recovery Act (‘NIRA’) into law, creating the Public Works Administration (‘PWA’) backed by USD3.3 billion to finance infrastructure projects; and reducing production in certain industries while raising workers’ wages via industrywide agreements.

- Restore the sense of a just society

- August 1935: FDR signs the Revenue Act which raises federal income tax rates to 75% on income of more than USD 1 million and introduced an inheritance tax. Known colloquially as the ‘Soak the Rich’ tax;

- August 1935: signs the Social Security Act into law, instituting welfare payments for unemployed workers and pensions for over 65s. Twenty-six million people sign up in the first four months.

Personality Traits

Arguably, none of this would have been possible without Roosevelt’s unique set of personal attributes and mantras, which enabled him to carry the electorate with him, winning not one but three landslide elections (the races for New York state Governor in 1930 and for President in 1932 and 1936). These characteristics defy classification but well bear listing. They include:

- Be bold, be active, be honest

- “The country demands bold experimentation. It is common sense to take a method and try it: if it fails, admit it and try another. But above all try something”;

- Inauguration speech 1933 – the nation “cries out for action, and action now”;

- In the first 100 days, he signed 15 major bills into law – to create a sense of movement towards restoring national prosperity;

- “Everything he learned about economics at Harvard was wrong” (Dallek p51);

- February 1937: FDR proposes expanding the Supreme Court from nine to 15 justices in order to overcome judicial opposition to the New Deal after the court had overturned sections of the Agricultural Adjustment Act.

- Communicate!

- July 1932: “I pledge you, I pledge myself, to a new deal for the American people”;

- March 1933: instituted twice-weekly press conferences;

- Instituted his fire-side chats 12 March 1933 (eight days post inauguration).

- Be optimistic

- Inauguration speech: “the only thing we have left to fear is fear itself – nameless, unreasoning, unjustified terror which paralyses needed efforts to convert retreat into advance”;

- Theme song for the 1932 Presidential campaign – “Happy Days are Here Again”.

- Show compassion

- “Aid to jobless citizens must be extended by government, not as a matter of charity but as a matter of social duty ... and to preserve our democratic form of government ... Modern society ... owes the definite obligation to prevent the starvation ... of any of its fellow men and women who try to maintain themselves but cannot because of conditions beyond their control”. This stood in sharp contrast to Mellon’s admonition to Hoover to “liquidate the farms, liquidate the banks, purge the rottenness from the system”.

- Don’t scare the horses

- Most interestingly, FDR encourages the nation to balance its books! “Liberal governments have been wrecked on the rocks of loose fiscal policy”; “He judged intuitively that initial policies that echoed traditional means and ends would do more to advance subsequent progressive actions than bold strokes at the start” (Dallek p142). Importantly, he then went on to run deficits in every year of his Presidency!

Figure 1. Devaluation and Inflation Under FDR

Source: Bloomberg; Between 1925 and 1939.

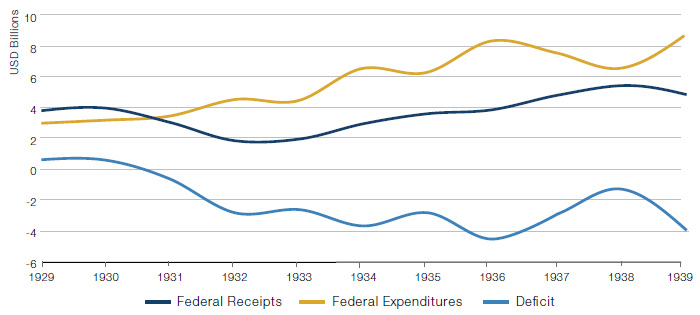

Figure 2. Nominal Federal Government Expenditures, Revenues, and Surplus/Deficit (1929-39)

Source: Federal government expenditures, revenues, and surplus/deficit are series Ea584, Ea585, and Ea586 from Wallis (2006, pp. 5-80 and 5-81).

Conclusion – Fire All Bazookas

Our over-riding sense is that it was the combination of determined monetary and fiscal stimulus applied simultaneously that really made the difference. Interestingly, there is no real scholarly consensus about the precedence of monetary or fiscal policy as the key ingredient of the recovery. Maynard Keynes himself visited the White House in 1934 and urged the President to maximise all possible government spending financed by loans, not by taxes – i.e. to increase the money supply. While M1 money growth did indeed accelerate from a 13% contraction in 1932 to over 10% growth in 1934-36, the government deficit was modest throughout the 1930s by today’s standards, being between 2% and 4% in nearly every year.

The three key lessons seem to be: 1) deploy every weapon in your arsenal to avoid deflationary slump; 2) re-jigging existing government spending to provide incomes for those with high marginal propensity to consume can provide a high multiplier fiscal boost, so very large deficits are not necessary; 3) keep applying the stimulus long after the crisis – the policy tightening of 1937 prompted a mini-depression and is widely seen as a mistake.

Let’s hope policymakers today can muster similar levels of conviction as FDR. We could all use some optimism.

You are now leaving Man Group’s website

You are leaving Man Group’s website and entering a third-party website that is not controlled, maintained, or monitored by Man Group. Man Group is not responsible for the content or availability of the third-party website. By leaving Man Group’s website, you will be subject to the third-party website’s terms, policies and/or notices, including those related to privacy and security, as applicable.