Key takeaways:

- We believe that deglobalisation is the most likely future path for the world, absent course-correcting forces. Under this scenario, the world splits into two or several major economic-technological spheres led by rival great powers

- We examine Deglobalisation alongside three alternative regime futures for the world order – Re-Americanisation, De-Americanisation and Fragmentation. Each carry materially different consequences for asset returns, inflation dynamics and portfolio construction

- Investors who recognise this regime shift, adapt their strategies and stay nimble may not only protect their portfolios, but potentially find ways to prosper in this new paradigm

Introduction

A year ago, we set out to determine whether the apparent retreat of globalisation was truly a structural transformation. We framed our enquiry around four core questions: how fast is the world deglobalising? How can we measure such a broad phenomenon rigorously? Over what horizon might a new equilibrium emerge, and how do we position portfolios for it?

We fused insights from political economy, data science and practical investment analysis. Leading political economist Professor Mark Blyth expertly anchored our thinking in theory and history. In parallel, researchers at the Oxford-Man Institute (OMI) and our Boston research centre built models to parse vast datasets and detect real-time shifts in economic activity and sentiment. In what follows, we translate our findings into scenario plans and strategic guidance for investors, including the potential implications of geopolitical developments year to date, principally the war in Iran.

Measuring deglobalisation

To interpret ‘deglobalisation’, we consulted an array of sources.1 We likened each era of global political economy to an operating system running on the hardware of institutions. The Gold Standard era (1870–1914), the Bretton Woods era (1945–1971), and the neoliberal globalisation era (1980–2016) were such systems, and each eventually broke down under internal stresses. The current period of deglobalisation, in our view, represents the system crash of the neoliberal order – the task now is to discern which operating system will reboot.

To translate this big-picture understanding into actionable analysis, we built a bespoke analytical toolkit which enabled us to comb through millions of data points across economies and markets to detect evidence of deglobalisation in real time. Advanced machine learning techniques (including natural language processing on news and policy documents) allowed us to learn the patterns associated with the peak of globalisation and its subsequent unwinding.

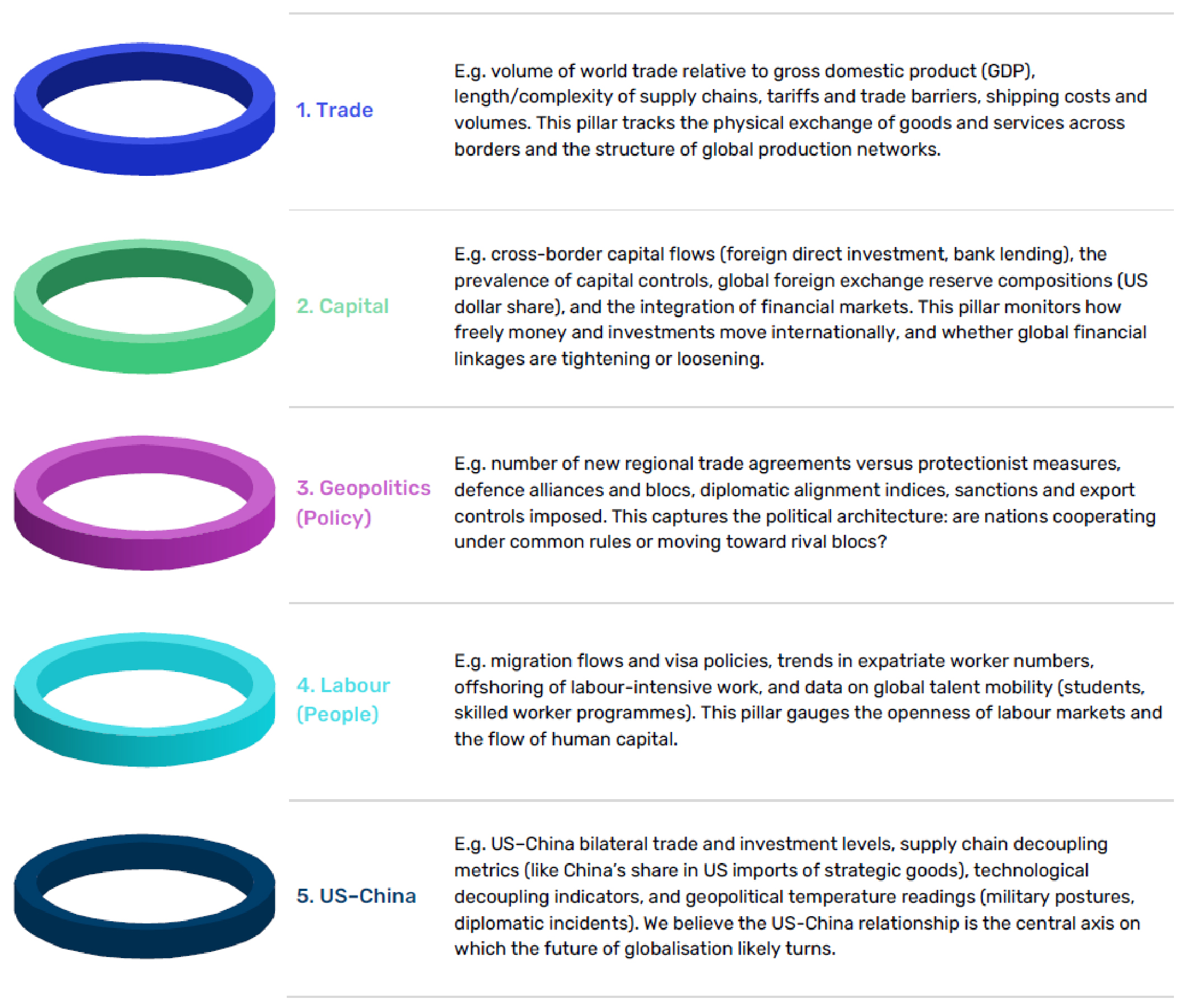

We distilled 77 key indicators that serve as a representative dashboard of deglobalisation, and then organised them under five pillars corresponding to the main domains of global economic integration.

Source: Man Group.

Our model and data pipeline also incorporate ‘nowcasting’ – using real-time data coupled with advanced statistical models to predict market and sales trends – and machine learning to fill in the gaps where official data is slow or insufficient. For example, where trade data is lagged by several months, the model uses shipping traffic trackers and corporate export order surveys to estimate current trade activity.

This five-pillar approach marries theory with a pragmatic, data-driven engine, enabling us to quantify deglobalisation with a level of precision and timeliness that traditional economic analysis cannot achieve.

How fast is the world deglobalising?

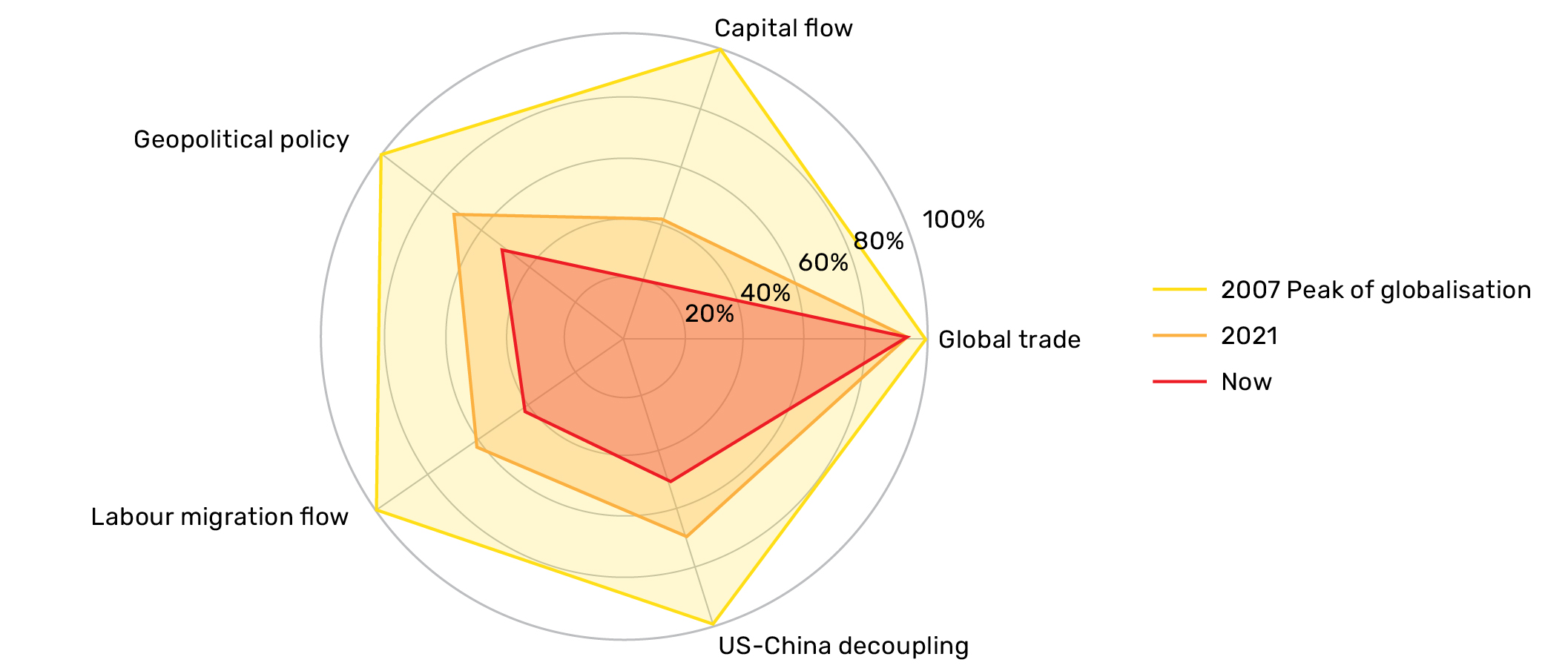

To translate our data-rich analysis into a decision-making tool, we created a ‘risk radar’ that quantifies the distance of the current global environment from the pre-2008 globalisation era across our five pillars. We chose 2007 as a baseline because by many metrics, the mid-2000s were the peak of global integration - trade as a share of GDP was at an all-time high, cross-border capital was abundant, geopolitical conflict was perceived to be at a minimum, labour flowed relatively freely, and US-China relations were still in deep economic engagement.

Figure 1. Deglobalisation risk radar

Source: Man Group. As of November 2025.

The risk radar matters because it forces us to think in terms relative to the 2007 peak-globalisation benchmark. Points near the outer ring mean the system still looks broadly like 2007; points pulled inward show how far we have moved away from peak globalisation. As the radar shows, some parts of the system are holding up, some are drifting, and others have undergone a profound break from the 2007 world.

In practical terms, the risk radar’s output can be mapped to investment risks: higher deglobalisation readings imply higher inflation risk (due to supply chain frictions, less labour arbitrage), higher political risk premia (as conflict or policy uncertainty rises) and potentially greater dispersion across markets.

While traditional macro indicators often lag (for instance, official foreign direct investment data might come annually with delay), the radar is a living model updated at least monthly. If, say, a new trade war erupts or a major geopolitical event occurs, its effects on our indicators will register in short order (indeed we have already seen this in 2026 following the US military action in Venezuela and then Iran). The risk radar has already confirmed that the world of 2026 looks very different from the world of 2007.

Where are we going?

To address this, we envisioned four distinct regime futures for the global order by the 2030–2035 horizon: Re-Americanisation, De-Americanisation, Deglobalisation and Fragmentation. These end-states are not predictions, but plausible scenarios grounded in our analysis of structural forces.

Figure 2. End-state scenarios

Source: Man Group.

These scenarios emerged from two primary axes of variation: (1) the degree of global openness versus closure, and (2) the degree of US centrality versus diffusion of power in the international system. In addition, we evaluated each scenario on dimensions such as whether international standards and institutions remain cohesive or diverge and the level of geopolitical conflict risk inherent in each world.

- Deglobalisation scenario: This is the current path, one of partial economic decoupling, but with the US still playing a significant (if reduced) role. Openness is low (trade and investment flows are significantly reduced or regionalised) and US centrality is medium – the world is split into multiple blocs, with the US leading one major sphere and a rival power (likely China) leading another. Standards cohesion is medium-to-low (each bloc has its own standards – for instance, a Western versus a Chinese tech stack). Conflict risk is low-to-medium: while outright war may be avoided via deterrence, rivalry could flare in proxy conflicts or cyber warfare.

For investors, the Deglobalisation scenario demands careful, bloc-wise strategies. Diversification benefits might increase, but cross-border investment opportunities shrink, and one should consider political risk (such as being forced to divest certain holdings, or the risk of capital controls between blocs). - Re-Americanisation scenario: A future in which the US reasserts a central leadership role and global integration recovers but with an industrialised, state capitalist flavour. Openness is medium and US centrality is high. In this scenario, standards remain largely cohesive (around Western norms) and conflict risk is low because the US-led order keeps major powers aligned or deterred.

For investors, Re-Americanisation would likely bring risk-on opportunities: emerging markets would broadly benefit from renewed capital flows, global supply chains would resume (albeit with some reshoring), and the US dollar would remain the linchpin. Importantly, this scenario assumes that the current deglobalising trends not only halt but reverse in many areas. This is a tall order. - De-Americanisation scenario: In this scenario, globalisation does not completely collapse – openness remains medium – but the leadership of the US diminishes significantly. Think of the US opting out of globalisation while the rest carry on as before. Power becomes more diffused across major players (China, Europe, India, perhaps regional leaders), without a single hegemon. Standards might fragment somewhat (medium cohesion) as different coalitions set their own norms. Conflict risk in this scenario is low-to-medium: outright great-power war is avoided, but there is persistent tension. Trade and capital still flow, but under a patchwork of regional agreements and digital spheres of influence.

De-Americanisation would require navigating a less dollar-centric world: portfolio diversification would need to account for the fact that correlations might decrease across regions. Opportunities might arise in markets that become new centres of gravity, but the absence of a single security guarantor could inject risk premiums in certain assets (e.g., energy routes subject to regional contestation, as we have seen of late). - Fragmentation scenario: This is essentially a breakdown of the global system. Openness is very low; protectionism and self-sufficiency dominate. US centrality is low. Standards cohesion is nil: different regions and even individual nations go their own way. Conflict risk in this world is high: without a stabilising superpower or cooperative framework, regional conflicts proliferate and even great-power military clashes become possible. Trade flows shrink dramatically (even within regions), capital stays mostly behind national borders, and information networks split apart. This scenario is the darkest – global growth would likely be dismal and volatility enormous.

For investors, this is a capital preservation scenario: it implies a need for maximum resilience, minimal reliance on cross-border assets, and a tilt toward hard assets or localised investments in relatively safe jurisdictions. Traditional diversification may fail (if most risk assets worldwide are down) – one would seek safety in real assets, commodities, or simply cash in the few stable currencies.

It is important to emphasise that these four end-states are ideal types – reality could contain elements of several.

Predicting the trajectory

Having defined four possible future regimes, we now ask which one are we headed toward? To answer this, we developed a probabilistic framework for extrapolating our data into scenario space. This involved taking trends from our 77 indicators and projecting them forward, while also incorporating the likely effects of policy momentum already in train (for instance, announced tariffs or demographic trends).

Figure 3. End-state model baseline, including Iran war overlay

Source: Man Group. As of 30 March 2026. This forecast is hypothetical, based on our proprietary models and current data, and is not a guarantee of future results.

Figure 3 shows how the modelled probability of each scenario has evolved since 1999, with forecasts out to 2035. Our model shows that, by 2020, the US-led global order was already much weakened. From the early 2020s onward, the baseline projection shows the Deglobalisation scenario as the highest trajectory, meaning our model currently sees the bifurcated-bloc world as the most likely end-state by 2030.

Since the development of our deglobalisation toolkit in 2025, much has already changed. While we could not have imagined that recent geopolitical events would unfold with such speed, our model had indicated the global trajectory.

In Figure 3, we have updated our 2025 end-state projections to account for the events of 2026 to date, principally the war in Iran. From 2026 onward, the dashed extensions track the pre-Iran war regime probabilities, whereas the solid lines show the post-Iran projections. The effect of the recent war2 is subtle yet meaningful: the future likelihood of Re-Americanisation lurches further downwards, and Deglobalisation trades some probability with the bleaker Fragmentation end-state. While our model still projects a deglobalised future, further degradation in the Global Trade and Geopolitical Policy pillars has contributed to a meaningful increase in the future risk of a fragmented world.

Another way to read the baseline projection is through the lens of risk management. Our current (post-Iran war outbreak) readings – roughly 50% Deglobalisation, 30% Fragmentation, 15% De-Americanisation, 5% Re-Americanisation3 – give a sense of risk-weighted scenarios to consider. In practice, this could mean stress testing portfolios for a baseline playbook of tariffs, sanctions, supply bifurcation and inflationary pressures, though a Deglobalisation world still has vibrant intra-bloc trade and likely rapid innovation as rival powers compete. The non-trivial tail risk of Fragmentation argues for maintaining hedges against more disorderly outcomes.

We must emphasise that these projections are not guaranteed. They are a simulation which is conditional on the trajectory as we see it today. In reality, big things can and will change – policy decisions, elections, technological breakthroughs. Our model provides a time series of regime probabilities that we can plug into stress tests, scenario work and ultimately portfolio construction. Instead of saying the world might be deglobalising, we can say, on our measure, that Deglobalisation is now the most likely projected outcome, and that its probability is rising fast. We can also show how different assets and strategies have behaved when that probability has been high or low. In short, it offers a disciplined way of translating the language of end states into the language of risk premia and allocation.

Portfolio implications for a new era

The final step is to apply regime probabilities to portfolio construction. For this, we combined the deep experience of our own investment professionals with the deglobalisation model, to assess which assets, sectors and styles could potentially be helped or hurt in each regime. The global economic landscape is transforming, and our job as investors is to adapt to its new structure.

Below, we share some thoughts as to what this might mean in practice:

- Portfolio construction: A shifting global economic regime calls for a re-examination of how portfolios are built, specifically through the lens of resilience and diversification. Higher inflation volatility could challenge fixed income returns, while new winners and losers will likely emerge in equities as geopolitics intrudes.

- Diversification: This must be thought of in broader terms, not just across asset classes and strategies, but across regimes and scenarios. This might involve allocating a portion of assets to strategies tailored for each of our four scenarios and avoiding over-committing to any single vision of the future. Consider diversifying by theme – targeting themes that transcend regimes, such as digitisation, decarbonisation or healthcare, but expressing them differently depending on the regime (e.g. localised renewable energy projects, versus global clean tech companies). Geographic diversification could also be crucial. Markets underrepresented in global portfolios today could become tomorrow’s growth engines if they manage to sidestep great-power conflicts.

- Liquidity: When opportunities or dangers suddenly emerge, liquidity allows investors to pivot. For instance, if capital controls or sanctions hit, illiquid positions in certain jurisdictions could become trapped; better to limit those or demand a higher premium for holding them. We see merit in a modest defensive tilt in the portfolio. This doesn’t mean abandoning growth but rather ensuring that in aggregate the portfolio can withstand inflation spikes, recessions or financial crises that might accompany the regime shift. This might mean a slightly higher allocation to real assets (real estate, infrastructure) which have intrinsic value and can act as an inflation hedge, or to gold and commodities as geopolitical hedges. It might also mean examining tail-risk hedges (options, insurance-like instruments): the cost of carry for such hedges in the calm times could pay off in the storm.

- Currency strategy: A structurally weaker or more volatile US dollar is a plausible outcome in a world where its exorbitant privilege is questioned. That said, we don’t foresee the dollar disappearing as the primary reserve; rather, a gradual erosion.

- Active engagement: Organisations might consider in-house geopolitical expertise or partnerships, much as they do with economic forecasting. Why? Consider how an ideological shift in Washington or Beijing could translate, with almost no lag, into changes in risk premia, capital expenditure schedules and market share.

- Active management: Simply owning the market index might expose one to undesirable concentrations. Skilled active managers can target or avoid companies overly exposed to deglobalisation risks. A less globalised world might also see more dispersion in returns – which is typically conducive to active alpha generation.

- Philosophical diversification: Biases might have accumulated during the long era of globalisation, such as an inherent belief that markets will self-correct, or that technology inevitably unites the world. Those assumptions are being tested. Scenario planning exercises force us to wear the hat of vastly different futures and consider how our strategies look in each.

Conclusion: adapting to thrive

Amid the cautious note struck in this paper, we must not lose sight of opportunities. Every regime shift brings new winners. For instance, a world of supply chain re-localisation is a boon for logistics, automation and industrial real estate in safe hubs. Deglobalisation is not an aberration to wait out; it is the probable new reality to confront and navigate. Long-term investors, with multi-decade horizons, are likely in a strong position: unlike short-term players, they can position capital today to benefit from the eventual next stable order.

Every major economic reboot in history, after a period of pain and adjustment, has eventually ushered in new prosperity. If today’s deglobalisation is our generation’s trial, it will likely spur innovations – perhaps in energy, automation, medicine – that form the bedrock of a more sustainable and inclusive future order.

If there is one takeaway, it is that in a time of transformation, adaptability is the supreme virtue. The investors who recognise the regime shift, adapt their strategies, and stay nimble might not only protect their portfolios, but potentially find ways to prosper in the new world being born.

AI was used to support data analysis and processing in the production of this article.

1. Among many others, we leaned on economic historian Karl Polanyi’s concept of the double movement and Jacques Attali’s vision of future world orders (writing in 2006, Attali predicted the eventual decline of US-led deglobalisation).

2. As at the time of writing, the Iran war is ongoing, albeit in a temporary ceasefire period.

3. Source: Man Group projections, as of 30 March 2026.

You are now leaving Man Group’s website

You are leaving Man Group’s website and entering a third-party website that is not controlled, maintained, or monitored by Man Group. Man Group is not responsible for the content or availability of the third-party website. By leaving Man Group’s website, you will be subject to the third-party website’s terms, policies and/or notices, including those related to privacy and security, as applicable.