The major technology companies are expected to spend an estimated US$650 billion on capital expenditure this year. Most of that money will likely flow to the usual suspects, such as the US hyperscalers building data centres and the chip designers pushing computing power ever higher.

But the physical wiring connecting those processors is reaching its limits, potentially threatening to choke further growth. Overcoming this bottleneck requires a fundamental shift in hardware, creating an opening for the European industrial specialists that manufacture the necessary components required to enable the next generation of architecture.

The problem

Training a frontier AI model now requires over a million chips working in parallel, exchanging data continuously. Anthropic's latest model reportedly cost around US$10 billion to train, which we estimate is roughly 30 times more than frontier models barely a year earlier.

However, this escalation exposes three existential problems:

- Failures multiply. A million-chip cluster experiences a hardware failure roughly every three minutes. At a US$10 billion training cost, even 5% lost computing power equals a waste of US$500 million

- The network becomes a bottleneck. Based on our conversations with a number of industry experts who test optical switches, the consensus appears to be that about 80% of data centre traffic is now chips talking to each other, and congestion means processors can sit idle for 20% to 30% of the time, waiting for data

- The energy cost is substantial, and network switching alone can consume around 15% of total data-centre power, according to our experts

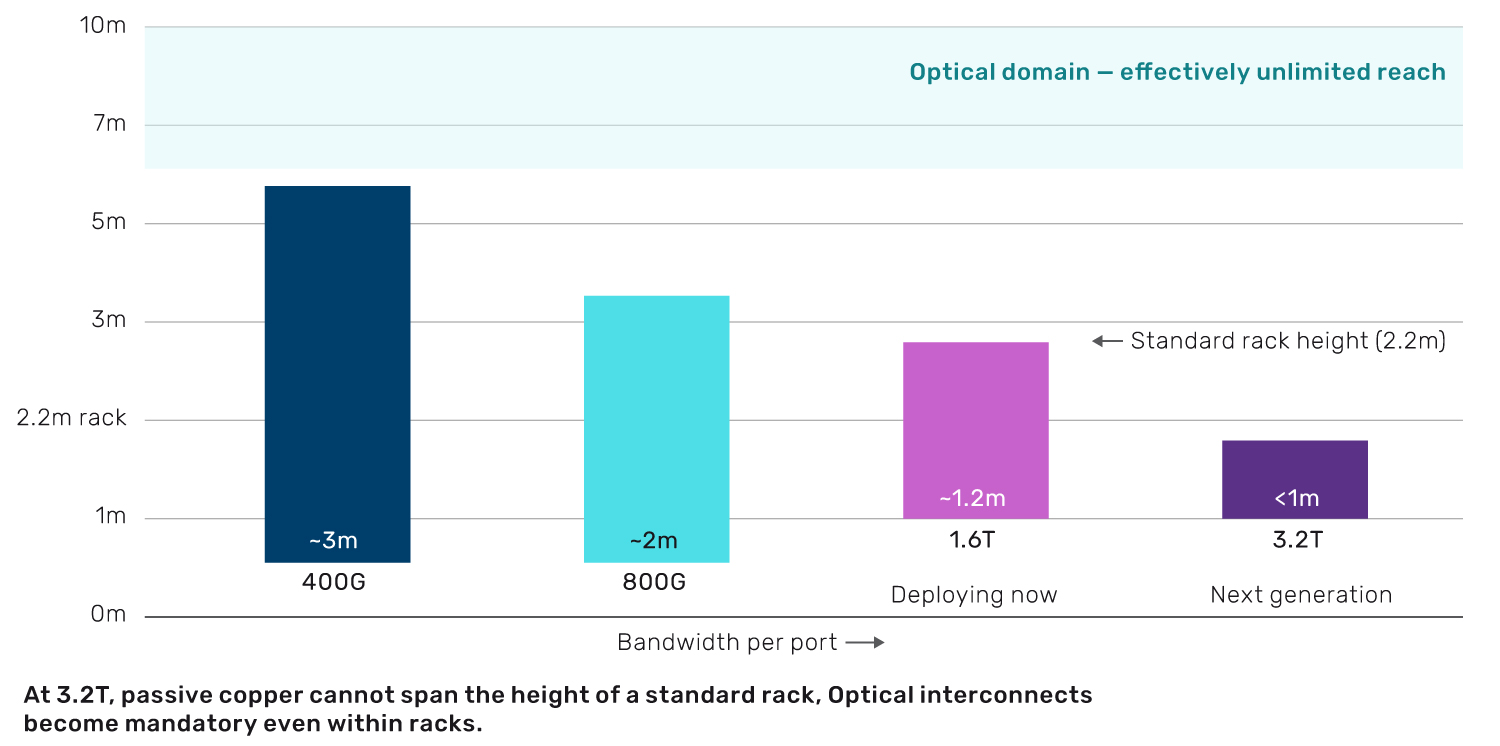

Compounding all three is a physical constraint the industry calls the copper wall (Figure 1). At the fastest speeds currently being deployed (1.6 terabits per second), copper wiring can no longer carry signals between server racks. At the next generation of speeds, it cannot reliably span even a single rack, and no software update will be able to fix this.

Figure 1. The copper wall

Source: Man Group analysis based on Lumentum OFC 2026 Investor Briefing. Passive copper (DAC) maximum reach at each data rate. For illustration purposes only.

The solution

The industry is making a wholesale shift from electrical to optical interconnects, transmitting data as light rather than electricity, which can address all three problems simultaneously.

Optical circuit switches redirect light between fibres to manage data-centre traffic, which can cut network switching power by 40% to 80%. Co-packaged optics bond photonic chips directly onto processors, which can reduce per-link power by up to 90%

The market

Both technologies are now moving from pilot projects to full-scale procurement by the hyperscalers and the market is projected to grow from US$18 billion in 2025 to over US$90 billion by 2030, roughly 40% annual growth.

At the heart of these optical links are lasers made from indium phosphide (InP), a compound semiconductor that generates the light carrying data between chips. This is a technology displacement already well underway. InP’s share of high-speed data centre optical lanes has risen from 44% in 2022 to 79% today, and is forecast to reach 91% by 2030.

The Europeans

While the biggest supplier of these most critical, hard-to-replicate capabilities is US-based Lumentum, we see a cluster of companies coming out of Europe that also make this transition possible.

The continent has deep strengths in photonics and compound semiconductor manufacturing, built over decades of research and industrial development. Switzerland's Huber+Suhner, the UK's Oxford Instruments and Germany's Aixtron for example make the optical switches, laser fabrication equipment and crystal growth reactors which sit at critical points in this supply chain.

In many cases, their competitive moat is built on proprietary process knowledge accumulated over decades of working with specific materials and customers. The equipment makers in particular benefit from a picks-and-shovels dynamic. It does not matter which laser company or hyperscaler wins the race downstream. Whoever builds the lasers needs the machines.

Looking ahead

The optics industry is also at an inflection point. Many of these suppliers are transitioning from equipping research labs and pilot lines to supplying full-scale production, a meaningful shift in the volume and recurring nature of the revenue.

As the physical limits of copper force a redesign of data centre architecture, Europe’s specialised industrials quietly supplying the infrastructure that makes it all work may offer investors a slightly different way to play the AI theme.

AI was used to support data analysis and processing as well as some early drafting in the production of this article.

Authors: Brentley Campbell, a portfolio manager covering European mid-cap stocks at Man Group and Isak Hirsch, an analyst covering European mid-cap stocks at Man Group.

You are now leaving Man Group’s website

You are leaving Man Group’s website and entering a third-party website that is not controlled, maintained, or monitored by Man Group. Man Group is not responsible for the content or availability of the third-party website. By leaving Man Group’s website, you will be subject to the third-party website’s terms, policies and/or notices, including those related to privacy and security, as applicable.