AI data centres and drought-stricken farmers could be about to start fighting over the same water and power. This year’s ‘Super El Niño’ has arrived and its landing on one of the key market drivers should shake investors out of their complacency around climate volatility.

El Niño is a naturally occurring climate pattern that drives up sea surface temperatures in certain regions and is commonly associated with extreme weather events. The National Oceanic and Atmospheric Administration confirmed its arrival in June, when sea surface temperatures across the central and eastern Pacific rose enough above average to cross the threshold, a shift that historically brings more extreme weather worldwide. The Climate Prediction Center expects it to keep strengthening through the Northern Hemisphere winter, with a real chance it becomes one of the strongest events on record, hence this year's event has been dubbed 'Super El Niño'. Ocean heat built up in that process tends to linger, so the weather impact could stretch well into 2027 rather than fade with the new year.

We believe markets have barely begun to price this risk, which for food and commodity prices skews mostly to the upside. El Niño lands on an already-stretched power grid, an already-tight liquefied natural gas (LNG) market, and a global food chain with little slack left, so heat, power, water, and crop shocks reinforce each other rather than staying contained.

The fertiliser chain reaction

Agriculture will likely be hit hardest, as shifting growing conditions tend to cut crop yields and push food prices higher. El Niño typically reduces agricultural yields by 5-12% in affected regions, with staples like rice down 2-8%. But the impact is uneven with tropical Asia likely carrying the most risk, while North America and southern South America can come through relatively unscathed. The deeper risk is how globalised the supply chain has become. Southern Brazil may see useful rain, but over 90% of its nitrogen fertiliser is imported, and its crop development depends as much on Chinese urea exports, themselves exposed to China's hydropower conditions, as on local rainfall. Grocery inflation is already forecast to rise more than 3% in 2026; a strong El Niño might add further upside risk, with estimates that food inflation could reach double digits by 2027. The crops most exposed are tropical, such as rice, coffee, cocoa and sugar, but the reach extends to Australian wheat output, livestock heat stress, and aquaculture nutrients

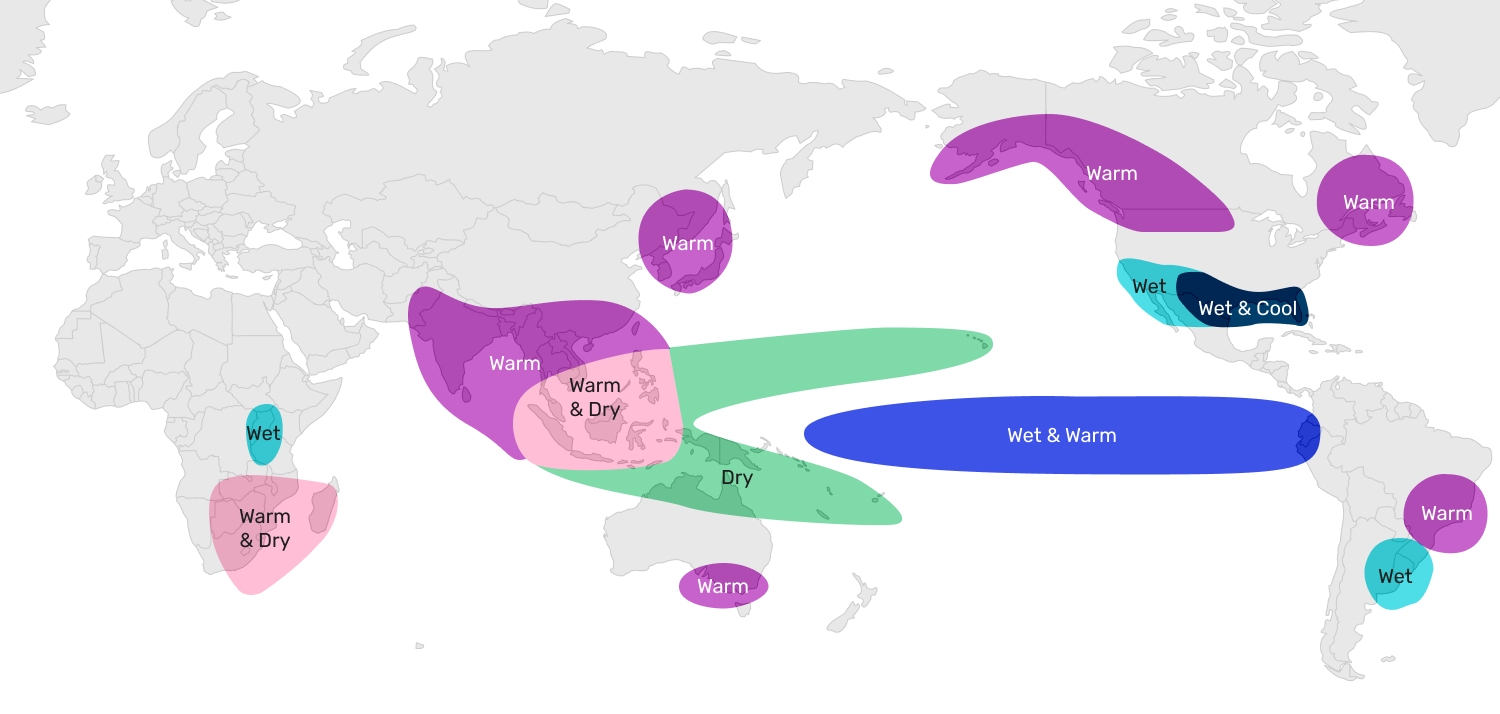

Figure 1a. El Niño effects from December through February (changes from normal weather)

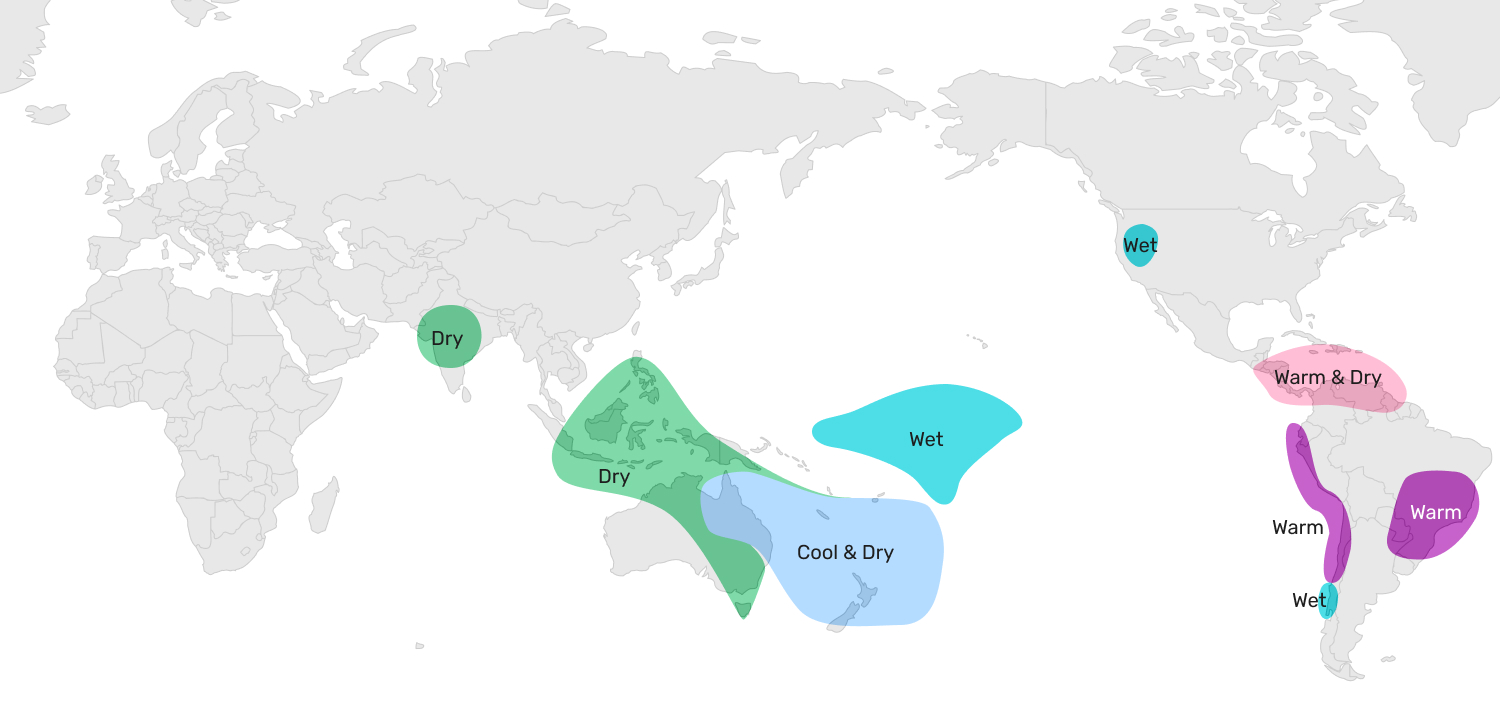

Figure 1b. El Niño effects from June through August (changes from normal weather)

Source: The National Oceanic and Atmospheric Administration, 2023 https://www.noaa.gov/jetstream/enso_impacts

Grid already at breaking point

Cooling demand from El Niño adds fresh pressure to a grid already straining under AI-driven load growth and rising electrification. Layer on ageing infrastructure across North America and Europe, and the risk is a grid pushed to its limits. El Niño should put grid investment back in focus for investors, not as an AI by-product, but as its own imperative. There is also a real risk this El Niño extends heat impacts into an even hotter 2027, building on a 2026 that is already on track for record heat. That should keep demand for natural gas and thermal coal elevated, just as global LNG supply remains constrained by Middle East outages.

Heat can often trigger water stress and volatility from floods in one region but droughts in another. Investors commonly think only of drinking water, but the vast majority of water is actually used for agricultural or food production, industries and power demand like hydro and nuclear generation (increasingly, cooling for AI data centres).

Hot metal

Metals aren't immune either. Copper production is highly water-intensive, and heat or drought conditions can tighten availability sharply. Aluminium is power-hungry in a different way; electricity accounts for 30-40% of production costs, and smelters depend on cheap, often hydro-generated power. Cooling, food production and AI growth are all set to compete harder for the same scarce power and water resources. Extreme weather compounds the disruption elsewhere too, from water transit chokepoints like the Panama Canal and the Rhine to the economic toll of wildfires, as seen in California.

When it rains, it pours

The real risk here is contagion: impacts rarely stay confined, and tail events usually come from several pressures compounding at once. Record heat can tighten gas supply just as drought curbs hydro power; tighter gas then limits nitrogen fertiliser output globally, while erratic growing conditions squeeze yields from the other direction. It's that intertwining that risks turning a weather event into a genuine shock.

Trading short-term weather is rarely a sustainable strategy, since forecasting edge is scarce and these events tend to be transitory. Not every El Niño has pushed food and commodity prices higher. But global supply chains already sit at a fragile crossroads of rising geopolitical dislocation and resilient demand, and history has shown how quickly that fragility surfaces once markets stop pricing in the risk.

We believe the real risk is to treat this El Niño episode as an idiosyncratic event – what if the current El Niño is only one point in an arc of events to come? Are investors chronically underpricing climate volatility as a systematic risk?

Author: Al Chu, a portfolio manager covering natural resources at Man Group.

You are now leaving Man Group’s website

You are leaving Man Group’s website and entering a third-party website that is not controlled, maintained, or monitored by Man Group. Man Group is not responsible for the content or availability of the third-party website. By leaving Man Group’s website, you will be subject to the third-party website’s terms, policies and/or notices, including those related to privacy and security, as applicable.