In this week’s edition: QE: absence makes the heart grow fonder; a Pyrrhic victory; and valuation spreads stretch.

In this week’s edition: QE: absence makes the heart grow fonder; a Pyrrhic victory; and valuation spreads stretch.

January 15 2019

Absence Makes the Heart Grow Fonder

All good things come to an end. For the equity markets at least, quantitative easing (‘QE’) has been the gift that kept on giving, supporting risk asset prices for the last 10 years.

2018 was the year things changed. Indeed, for five of the 12 months of the year, the world’s top 10 central banks cut the size of their aggregate balance sheet. As we have previously discussed, this creates a need for a ‘step-up’ by the private sector assets which would have been purchased by central banks instead need to be purchased by market participants.

In response, equity markets reacted badly. In January 2018, the top 10 central banks cut the size of their balance sheets by $37 billion; the S&P 500 Index then fell 4% in February. In March, the balance sheet reduction was $3 billion. The S&P 500 fell by 3% during the same month. In September and October combined, the reduction was $135 billion, while the index fell 7% in October. Full data is yet to become public, but we estimate that for December, balance sheet reduction was $60 billion, with a corresponding fall of 9% in the S&P 500.

As central banks look to tighten further in 2019, asset managers may yet pine for the good old days of QE.

Valuation Spreads Stretch

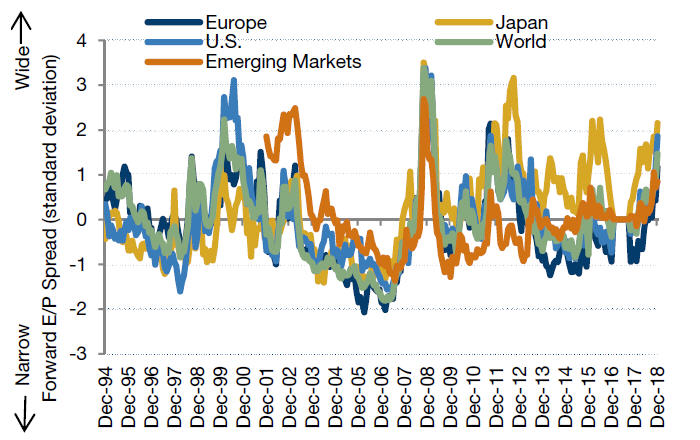

Valuation spreads, or the difference between the most expensive and cheapest stocks, ballooned in the fourth quarter of 2018. This was evident across all regions. Notably, spreads in Europe are approaching levels last seen during the sovereign debt crisis.

This widening of spreads acted as a headwind for value investors in the quarter because it implies that market participants are willing to continue to pay for expensive names and were not rewarding cheap stocks1.

However, the widening of spreads also sets up an opportunity for mean reversion. Indeed, as Figure 1 shows, during heightened periods, the spread widening acts like a coiled spring. When the spread snaps back, it can do so at a very fast pace, and value stocks can then come into favour very quickly.

Figure 1: Global Valuation Spreads Widen

Source: Man Numeric, Bloomberg; As of December 31, 2018.

Standardized spread between the current forward Earnings/Price spread and forward Earnings/Price spread since inception (developed markets 1995, emerging markets 2002).

Europe, Japan, US, and World are represented by the largest 400 names per region by market cap. Emerging Markets are represented by Man Numeric’s full stock selection universe for EM Core, which is approximately 3,600 of the most liquid EM stocks, including all of those in the MSCI EM Index.

A Pyrrhic Victory?

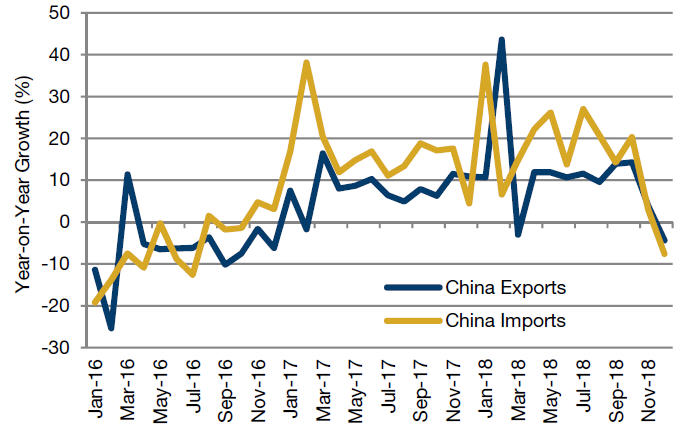

A domestic slowdown and a trade war with the US resulted in Chinese exports declining 4.4% in December from the previous year, the most in two years, while imports fell 7.6%.

We have previously discussed how any recovery in China’s economy will be more ‘L’ shaped than ‘V’, so the fall in trade data does not take us entirely by surprise.

However, what these figures do is provide a new perspective on ongoing trade negotiations between China and the US. President Donald Trump has indicated that any deal will require China to increase purchasing of US goods. Even if China buys more from the US in percentage terms, if the Chinese economy slows down, the dollar value of Chinese purchasing from the US could drop. Any gains to the US economy from the trade deal may therefore be ephemeral in the face of a turn in the Chinese economic cycle.

Figure 2: Chinese December Exports, Imports Numbers Disappoint

Source: Bloomberg, as of January 2019

With contribution from: Henry Neville (Man Solutions, Analyst), Rob Furdak (Man Numeric, Co-CIO) and Matthew Sargaison (Man AHL, Co-CEO).

1Value stocks are defined as the 20% with the highest forward E/P ratio.

You are now exiting our website

Please be aware that you are now exiting the Man Institute | Man Group website. Links to our social media pages are provided only as a reference and courtesy to our users. Man Institute | Man Group has no control over such pages, does not recommend or endorse any opinions or non-Man Institute | Man Group related information or content of such sites and makes no warranties as to their content. Man Institute | Man Group assumes no liability for non Man Institute | Man Group related information contained in social media pages. Please note that the social media sites may have different terms of use, privacy and/or security policy from Man Institute | Man Group.