In this week’s edition – Reasons to buy value; and why rate hikes in the euro area are not imminent.

In this week’s edition – Reasons to buy value; and why rate hikes in the euro area are not imminent.

November 6 2018

Reasons to Buy Value

As the value versus growth debate continues, we look at two reasons why we feel value could outperform growth.

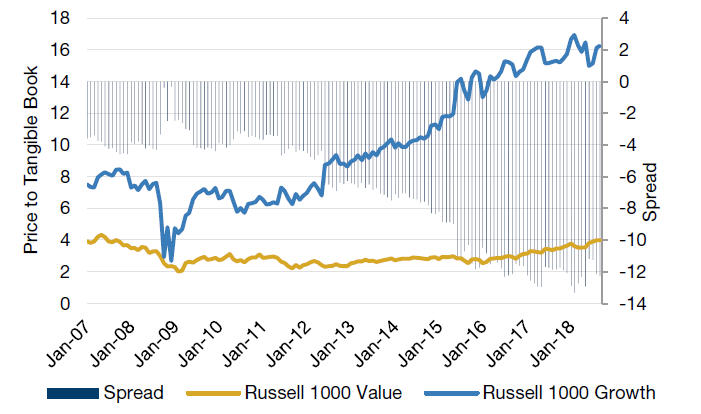

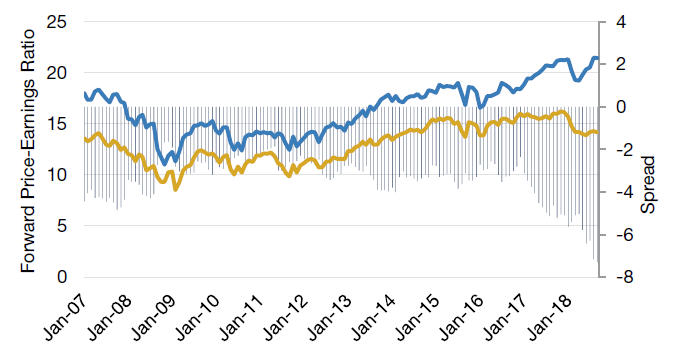

First, value is cheaper. Ten years ago, the price-to-tangible book (P/B) of the Russell 1000 Value Index was 3.9 times, while the Russell 1000 Growth Index was at 7.5 times – a 3.6-point spread. Today, the P/B of the Russell 1000 Value Index is 4.0 times, similar to 10 years ago. However, the Russell 1000 Growth Index is 16.3 times today, a 12.3-point spread (Figure 1)! Additionally, on a forward price-to-earnings (P/E) basis, the Russell 1000 Value Index is at the cheapest level since 2006 relative to the Russell 1000 Growth Index (Figure 2).

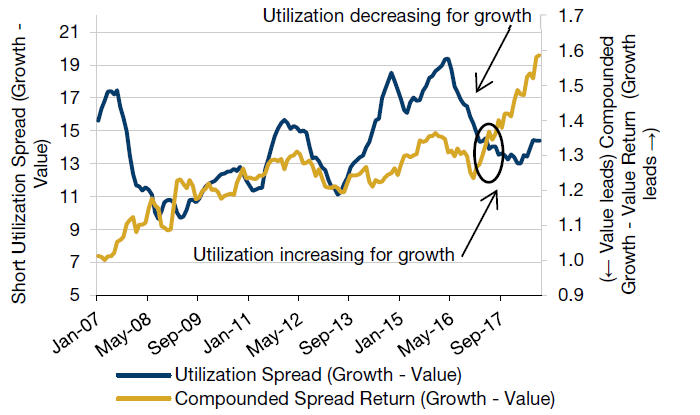

Secondly, short utilization has recently seen an uptick for growth stocks. The Russell 3000 Growth/Value short utilization spread is currently at 14.4%, i.e. 14.4% more of the lendable shares are being borrowed for the Russell 3000 Growth (R3000G) than the Russell 3000 Value (R3000V). This short utilization measure peaked at 19.4% in June 2016 (Figure 3).

Figure 1. Value is Cheap on a P/B Basis…

Source: Man Numeric, Russell, Bloomberg; as of September 30, 2018

Figure 2. …And on a P/E Basis

Source: Man Numeric, Russell, Bloomberg; as of September 30, 2018

Figure 3. Short Utilization versus Market Performance; Russell 3000 Growth and Value*

Source: Man Numeric, Russell, DataExplorers; as of September 2018 * Note: Utilization Spread = difference between utilization of R3000G – R3000V, Spread Return = Compounded spread between R3000G and R3000V

Rate Hikes? Really?

A perennial subject of debate is if, and when, the European Central Bank (‘ECB’) will hike interest rates. It is important to consider the overarching mandate of the ECB when thinking about this topic.

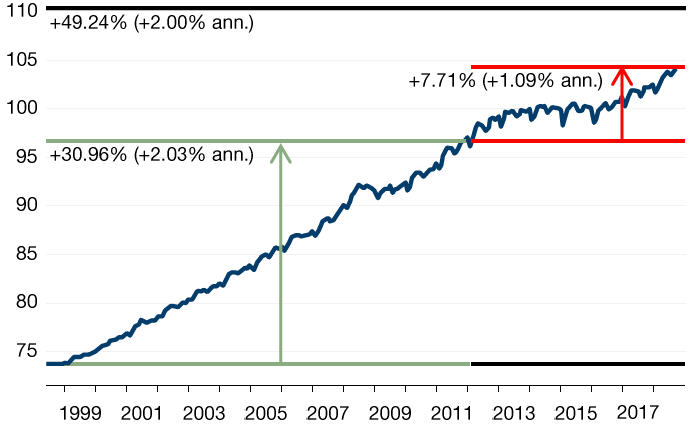

Unlike the Federal Reserve, the ECB only has one primary monetary policy objective: that of maintaining price stability. This was defined by the Governing Council as inflation “below but close to 2% over the medium term”1 . Figure 4 shows the harmonized CPI for the Eurozone. Between the inception of the ECB on June 1, 1998 and November 2011 (when Mario Draghi became president of the ECB), inflation increased at an annualized rate of 2.03%. Since 2011, inflation has only increased at a 1.09% annualized rate, well below their mandated target.

Given the discrepancy between actual inflation and the target, we find it hard to imagine that the ECB will have any incentive to hike interest rates until we see concerted inflationary pressure in the Eurozone.

Figure 4. Monetary Union Index of Consumer Prices (Eurozone Harmonized Inflation, All Items)

Between June 1998 and October 2018

Which Is Wrong – Equity Markets or Inflation Expectations?

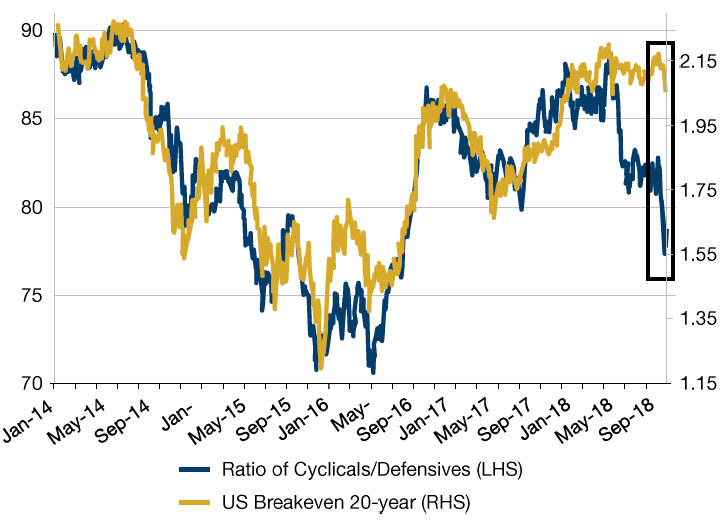

The US 10-year inflation breakeven has previously been positively correlated to the ratio of cyclicals to defensive. However, this relationship has broken down in recent months, as Figure 5 shows.

So, is the equity market getting it wrong? Or are inflation expectations going to catch up to reality?

Indeed, the equity market has previously seemed to predict recessions that never materialized. One more time?

Figure 5. Correlation Breakdown

As of October 31, 2018

Risk-Off Mode On

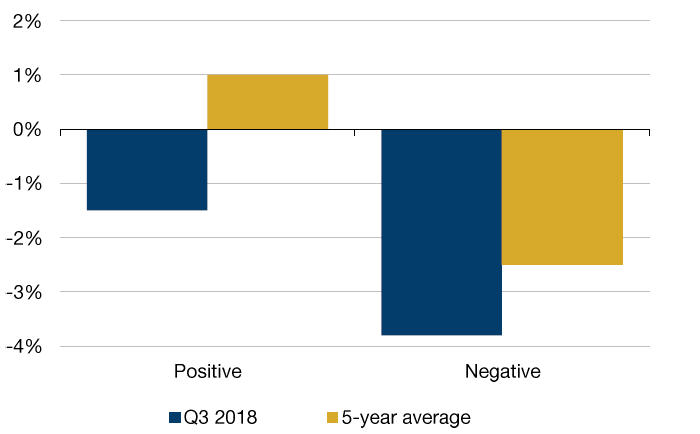

As of October 26, about half (48%) of the companies in the S&P 500 Index had reported their third-quarter results, according to Factset. So far, the companies whose results have been good, or at least in-line, have been sold off, while those companies who have had bad results have been heavily sold off. This implies to us that markets are in a risk-off/correction mode.

Indeed, those companies which reported positive earnings surprises saw a decrease in price of 1.5%, on average, from two days before the company reported actual results through two days after the company reported actual results, according to Factset. This compared with an average 1% increase during this 4-day window over the past five years. For the companies that reported negative earnings surprises, share prices declined 3.8% over the 4-day window, compared with a 5-year average of a fall of 2.5%.

Figure 6. S&P 500 Earnings Surprises Versus Average Price Change

Source: Factset; as of October 26, 2018

With contribution from: Pierre-Henri Flamand (Man GLG, CIO), Rob Furdak (Man Numeric, Co-CIO), Jeremy Wee (Man Numeric, Senior Portfolio Manager), Ethan Gao (Man Numeric, Associate Portfolio Manager), Ben Funnell (Man Solutions, Portfolio Manager) and Priyan Kodeeswaran (Man GLG, Portfolio Manager)

1https://www.ecb.europa.eu/mopo/strategy/pricestab/html/index.en.html

You are now exiting our website

Please be aware that you are now exiting the Man Institute | Man Group website. Links to our social media pages are provided only as a reference and courtesy to our users. Man Institute | Man Group has no control over such pages, does not recommend or endorse any opinions or non-Man Institute | Man Group related information or content of such sites and makes no warranties as to their content. Man Institute | Man Group assumes no liability for non Man Institute | Man Group related information contained in social media pages. Please note that the social media sites may have different terms of use, privacy and/or security policy from Man Institute | Man Group.