The signal emanating from around the world; and fund flows and their implications.

The signal emanating from around the world; and fund flows and their implications.

November 12 2019

When the US Sneezes…

In August, we noted that the US seemed poised for an equity uptick. According to our indicators, the combination of relatively compressed multiples equity valuations (largely valuation multiples), fundamentals (earnings revisions, margins and the cost of borrowing), and risk (investor sentiment and liquidity metrics) signalled the probability of an equity upswing.

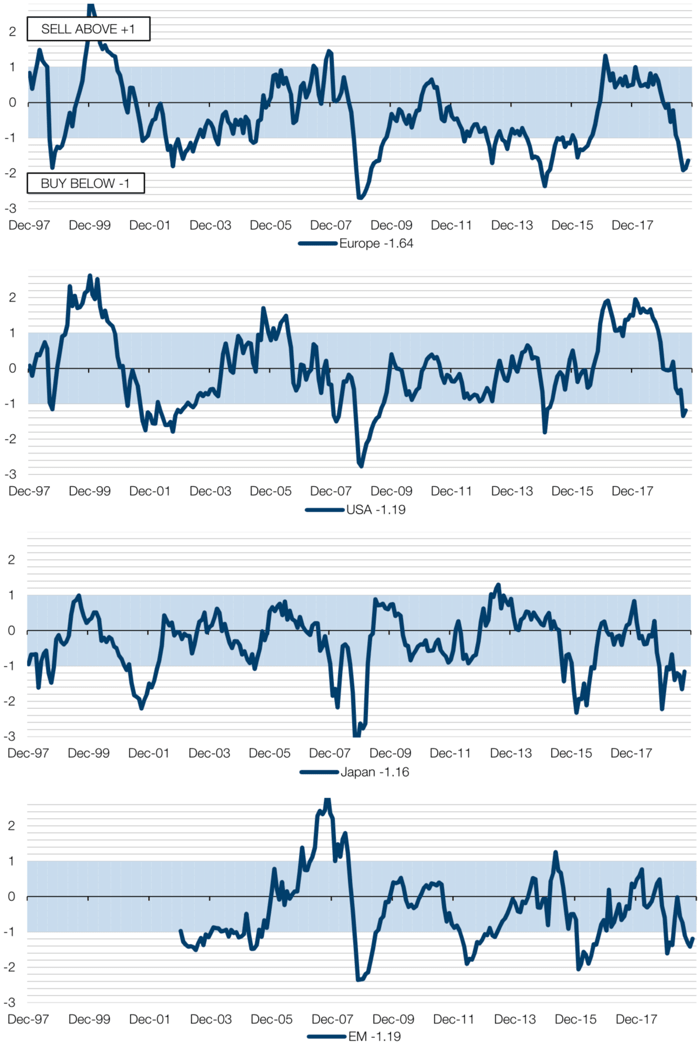

Drilling into the Valuation component, our CVI models are now showing a ‘buy’ signal across all geographies (Figure 1). For clarification, a market is deemed ‘buy’ territory when the above factors combine to drive the indicator below a reading of -1.

In our view, this is a welcome support of what we have written about previously: we may have another mini-cycle within this long, long bull market.

Figure 1. Composite Value Indicator

Source: Man Solutions; as of 8 November 2019.

Going With the Flows

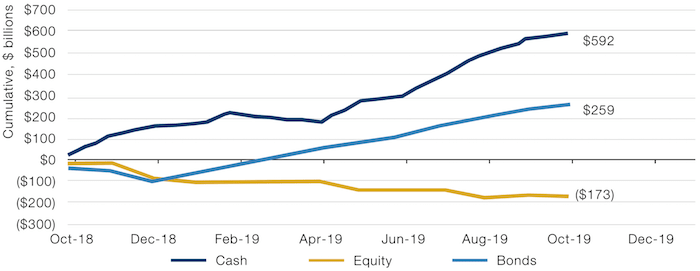

US equity funds have experienced USD100 billion of outflows during 2019 (Figure 2). Around USD217 billion has been withdrawn from active funds, with USD117 billion redirected into passives. This represents the second largest equity outflow in 15 years, and the largest spread between equity and bond inflows since 2008.

Despite the outflows, equity allocations remain high by historic standards (Figure 3), in the 81st percentile since 1990. Flows into bonds have reached the 50th percentile over the same period. Cash, despite increased allocations, remains very low by historic standards.

So, while investors may be de-risking, they are doing so from a very high starting point. In our view, we are a very long way from a headlong flight from equities.

Figure 2. US Fund Flows During Past 12-Months

Source: EPFR, Goldman Sachs; as of 24 October 2019.

Figure 3. The Recovery of the Eurozone Labour Market

| Equity | Debt | Cash | ||||

|---|---|---|---|---|---|---|

| Percent of total assets | ||||||

| Holder | Current | Percentile since 1990 | Current | Percentile since 1990 | Current | Percentile since 1990 |

| Foreign investors | 50% | 80% | 38% | 32% | 7% | 3% |

| Households | 38% | 78% | 21% | 52% | 15% | 22% |

| Mutual funds | 54% | 63% | 26% | 67% | 18% | 14% |

| Pension funds | 50% | 45% | 27% | 39% | 2% | 1% |

| Total | 44% | 81% | 26% | 50% | 12% | 5% |

Source: Federal Reserve, EPFR, Goldman Sachs; as of 24 October 2019

With contribution from: Ben Funnell (Man Solutions, Portfolio Manager), Teun Draaisma (Man Solutions, Portfolio Manager), Henry Neville (Man Solutions, Analyst) and Rob Furdak (Man Numeric, Co-CIO).

You are now exiting our website

Please be aware that you are now exiting the Man Institute | Man Group website. Links to our social media pages are provided only as a reference and courtesy to our users. Man Institute | Man Group has no control over such pages, does not recommend or endorse any opinions or non-Man Institute | Man Group related information or content of such sites and makes no warranties as to their content. Man Institute | Man Group assumes no liability for non Man Institute | Man Group related information contained in social media pages. Please note that the social media sites may have different terms of use, privacy and/or security policy from Man Institute | Man Group.