Introducing climate change in portfolios is not without its challenges, but we believe solutions exist.

Introducing climate change in portfolios is not without its challenges, but we believe solutions exist.

May 2019

Introduction

Climate change, and how to address it, within investment strategies are becoming ever more important for investors, money managers and financial regulators alike. Indeed, climate change was considered to be the most important specific environmental, social and governance (‘ESG’) issue by money managers, according to the US SIF Foundation.1 For institutional investors, climate change was the third-most important issue.

While most of the attention so far has been on whether controls on carbon emissions will strand the assets of fossil-fuel companies2, we believe it is important to widen that net and look at climate change across an investment portfolio.

Climate-change investing follows two main principles. First, climate-change investors seek to invest in those companies which make a positive contribution to combatting climate change. Second, climate-change investors seek to strengthen their portfolios against the future environmental, political and social effects of climate change.

In this article, we explore the three main challenges investors encounter when aiming to introduce climate change into their discretionary portfolios – engagement versus divestment; the lack of data; and tracking error – and how to address them.

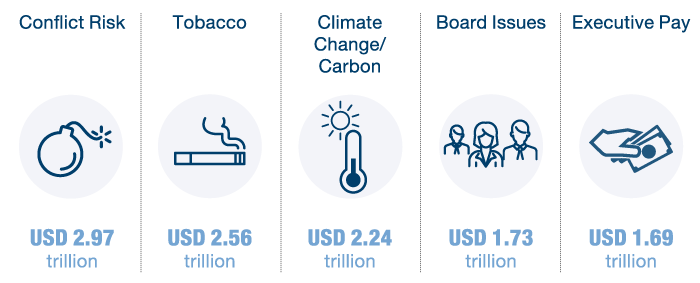

Figure 1: Top Specific ESG Criteria for Money Managers 2018

Figure 2: Top Specific ESG Criteria for Institutional Investors 2018

Source: US SIF Foundation's 2018 Report on US Sustainable, Responsible and Impact Investing Trends.

Challenge 1: Engagement Versus Divestment

Perhaps the most important conundrum in climate-change investing is the engagement versus divestment debate. (Indeed, this debate is something that comes up over and over again. Listen to what Harvard Management Company’s Michael Cappucci and Fiona Reynolds, the CEO of the UN Principles of Responsible Investment, have to say on this matter in our ‘Perspective Towards a Sustainable Future’ podcast series).

Traditionally, social responsible investing (‘SRI’) has incorporated the use of negative screening to avoid investing in sectors which are controversial. Using this framework, climate-change investors would divest themselves of anything related to polluting industries, selling oil companies, mining firms, auto manufacturers and other emissions-producing firms.

Whilst this approach helps avoid the perceived moral contagion of owning controversial stocks, it doesn’t necessarily help to promote better behaviour within these sectors. Deciding to exclude any particular industry requires qualitative judgement and also reflects the interaction of wider ESG factors with climate-change investing. Managers might consider some sectors to be entirely irredeemable.

By contrast, some highly polluting sectors are arguably indispensable to a green economy. Improved battery technology is essential if we are to replace the world’s reliance on fossil fuels. However, these batteries use lithium, alongside large quantities of nickel and graphite. Nickel mining has had a bad reputation in recent years; the Philippines closed 17 nickel mines in 2017 due to environmental concerns, especially deforestation.3 This leaves the climate-change investor in something of a quandary – by supporting a key part of the supply chain for electric vehicles, one might actively contribute to deforestation.

In our view, the way forward is to be actively engaged with sector-leading companies to encourage better practices from the sector as a whole. By using ratings to provide a screen, investors could then create portfolios weighted toward companies who are ESG leaders within their sectors. This could help avoid restricting the investment universe, and allow for engagement. Nickel mining in the Philippines is again a good example; in September 2018, the government introduced rules to ensure companies re-forested land they had worked.4 If prepared to engage with mining companies, environmentally conscious investors could contribute to similar initiatives and improve the impact of the sector as a whole. To set up the portfolio in this manner, managers would operate a positive rather than a negative screen, actively seeking out companies with stronger ratings and assisting them to improve further.

With engagement, responsible investors can actively vote at companies’ annual (or extraordinary) general meetings, for example, to improve ESG policies and behaviours. Indeed, shareholders can mandate corporate disclosures on a number of issues, such as improving the quality and timeliness of emissions data, assessing the environmental risks in the company’s business model and mandating disclosure of other sustainability metrics such as water usage and energy efficiency. One such example is oil major Royal Dutch Shell, which – in December 2018 and after discussions with institutional investors acting on behalf of Climate Action 100+ – agreed to link executive pay to short- and long-term targets for reducing carbon emissions.5 Additionally, a shareholder vote in May 2018 required natural gas company Range Resources to issue a report on its policies related to methane emissions and management.6 By enhancing disclosures, investors highlight environmental issues, whilst the data released can be used to form a more accurate assessment of company performance.

A key point to note is how important institutional investors can be in effectively advocating change. In ‘Political, Social and Environmental Shareholder Resolutions: Do they create or destroy shareholder value?’, Joseph Kalt and Adel Turki detail the increase in the number of activist resolutions filed on environmental issues, from 51 in 2006 to 100 by July in 2018.7 However, only four climate change-related proposals passed in shareholder meetings between 2006 and 2017.8 Of these, the paper analyses the three successful proposals which occurred in 2017, which required Occidental Petroleum, Exxon Mobil and PPL to publish assessments of the impact of climate change on their business in the event of global warming in the range of 2 degrees Celsius. Tellingly, all three successful proposals were supported by institutional investors.

Indeed, in their paper, Kalt and Turki say that without the votes of these three asset managers, the proposals would not have passed. Retail investors only voted 10% of their shares in favour of all environmental proposals in 2017, compared with 32% of asset managers. We believe asset managers using their concerted voting power will continue to provide the best chance of changing corporate behaviour on environmental issues.

Man GLG currently assesses how a proposal may enhance or protect shareholder value in either the short, or long, term when deciding how to vote. Considerations of climate change and ESG remain a factor within this framework. Over time, we hope to continue to use these shares to better promote good governance and sustainability, and to support initiatives that improve the environmental performance of companies in our portfolio.

Challenge 2: Data (Or the Lack Thereof…)

While there has been a leap in the quality and quantity of ESG data in recent years, disclosing, reporting and aggregating ESG data still remains a significant challenge, not just to climate-change investors, but to responsible investors generally. Complaints about ESG data often centre around:

- Absent or incomplete data;

- Data that is available, but incomparable across firms, industries and sectors;

- Too much unnecessary and/or irrelevant information;

- High cost of obtaining the data.

At Man GLG, we currently use two main data providers: Trucost and Sustainalytics. Trucost, a part of S&P Global, provides company ratings based on carbon emission data, alongside information on water use, pollution impacts and waste disposal. Sustainalytics also provides carbon portfolio analytics, alongside wider ESG ratings such as diversity, labour concerns and governance analysis.9

Both firms use proprietary models to create a sector benchmark for climate change performance, against which to compare corporate disclosures.10 However, models to produce final ratings rely on disclosures from companies about their supply chain and production methods as large inputs. As such, investors should beware of greenwashing. The 2015 auto emissions scandal provides a perfect example of how companies can disclose incorrect environmental data. It therefore remains vital that investors are able to conduct their own environmental due diligence alongside that of environmental data providers. Indeed, these vagaries can create potential opportunities for generating alpha for those willing to do detailed research. Man Numeric for example, is in the process of creating its own proprietary model to assess companies on their sustainability.

As well as scoring companies on their impact on the environment to promote change, responsible investors have to understand the potential impact of climate change on companies’ business models. In this area, the FSB Task Force on Climate-related Financial Disclosures (‘TCFD’) is making strides by encouraging companies to voluntarily disclose climate-related information. It also advises companies to disclose the governance, strategy, risk management tools and the metrics and targets they are using to try and manage the impact of climate change.

Again, this presents some challenges: Given that even leading climate scientists are unable to predict the pace of climate change with accuracy, it is difficult for non-experts to assess how climate change will affect their business. Secondly, it takes time to develop consistent standards. For context, the International Financial Reporting Standards (‘IFRS’) were first published in 2001, more than 30 years after the concept of international accounting standards was first mooted. Granted, climate change is a pressing issue, so it is possible that TCFD standards will become widely adopted more quickly than IFRS.

Challenge 3: Tracking Error and Carbon Pricing

Investing in climate-friendly companies also presents the problem of tracking error – the potential for green portfolios underperforming relative to their benchmark indices.

A smaller investment universe is often thought to lead to a higher tracking error, and vice versa.

This leads us to the question: do green portfolios actually underperform conventional benchmarks? To answer that, we compared the performance of the MSCI Low Carbon Target Index with the MSCI ACWI Index (Figure 3). Since 3 December, 2010, the MSCI Low Carbon Target Index has outperformed the MSCI ACWI Index by 44 percentage points.

Problems loading this infographic? - Please click here

Source: Bloomberg; as of 22 May 2019. *Normalised to 100 on 3 December 2010.

However, even if a low-carbon portfolio underperformed or generated similar returns to a conventional index, that could mean investors essentially get a free option on carbon. We believe that by investing in low-emission companies when their environmental status may be undervalued by the market, investors could benefit if the full cost of being a highly polluting company is eventually realised and incorporated into share prices.

Problems loading this infographic? - Please click here

Source: Bloomberg; as of 23 May 2019.

Conclusion

Christiana Figueres – best known for her successful coordination of the Paris Climate Agreement in 2015 – once said that “climate change increasingly poses one of the biggest long-term threats to investments.”

At Man GLG, we believe that climate change is a threat, but also an opportunity. Introducing climate change in portfolios is not without its challenges, but we believe solutions exist; and by introducing climate change in portfolios, money managers and investors can work with a forward-looking vision together to try and achieve more sustainable growth.

1. US SIF Foundation’s biennial Report on US Sustainable, Responsible and Impact Investing Trends, published October 2018: https://www.ussif.org/files/US%20SIF%20Trends%20Report%202018%20Release.pdf

2. Dietz, Bowen, Dixon & Gradwell, Climate value at risk of global financial assets, Nature Climate Change, April 2016.

3. https://www.reuters.com/article/us-philippines-mining/philippines-to-shut-half-of-mines-mostly-nickel-in-environmental-clampdown-idUSKBN15H0BQ

4. https://www.reuters.com/article/us-philippines-mining/philippines-implements-fresh-nickel-mining-curbs-in-environment-protection-drive-idUSKCN1LM0KY

5. https://www.shell.com/media/news-and-media-releases/2018/leading-investors-back-shells-climate-targets.html

6. https://www.pionline.com/article/20180517/ONLINE/180519842/shareholders-ok-proposal-calling-on-range-resources-to-issue-emissions-management-report

7. https://mainstreetinvestors.org/wp-content/uploads/2018/06/ESG-Paper-FINAL.pdf

8. Page 25, https://mainstreetinvestors.org/wp-content/uploads/2018/06/ESG-Paper-FINAL.pdf

9. https://www.sustainalytics.com/esg-ratings/

10. https://www.trucost.com/trucost-blog/rate-raters-uncovering-best-practice/

You are now exiting our website

Please be aware that you are now exiting the Man Institute | Man Group website. Links to our social media pages are provided only as a reference and courtesy to our users. Man Institute | Man Group has no control over such pages, does not recommend or endorse any opinions or non-Man Institute | Man Group related information or content of such sites and makes no warranties as to their content. Man Institute | Man Group assumes no liability for non Man Institute | Man Group related information contained in social media pages. Please note that the social media sites may have different terms of use, privacy and/or security policy from Man Institute | Man Group.