This year’s rally has been driven by six ‘puts’, in our view. All show how far policymakers could go to avoid disruption. None are a solution.

This year’s rally has been driven by six ‘puts’, in our view. All show how far policymakers could go to avoid disruption. None are a solution.

June 2019

Introduction

Politicians, once in power, hate volatility. This might seem a truism – after all, politicians usually come into power because of volatile situations. It is this fear of volatility that goes a long way to explaining the recent bull run we have seen, in our view.

At the beginning of 2019, we highlighted the possibility of a relief rally this year after the bloodbath of the fourth quarter of 2018; for every downside scenario we could think of, we highlighted possible policy reactions.

In our view, the rally has been based only partially on fundamentals. Instead, we believe it has been driven more by six ‘puts’ that have been handed to investors. In this case, we define a put as a policy decision designed to avoid instability in politics or the financial markets.

All of the puts have highlighted the level of pain that policymakers are prepared to tolerate, and the lengths they will go to avoid disruption, either of the economy, political life or both. None of the puts is a long-term solution to the underlying problems they seek to mask.

The Powell Put

The first put (of a short-term nature) is the end of the Federal Reserve’s rate hiking cycle. On 3 October, Fed chairman Jerome Powell described the “extremely accommodative low interest rates that we needed when the economy was quite weak” as unnecessary and “a long way from neutral”.1 The S&P 500 Index then proceeded to fall more than 6% until 28 November, when Powell backtracked and said interest rates were only “just below” neutral.

The Fed hiked rates by 25 basis points on 19 December. Almost five months later, the Federal Open Market Committee has committed to being “patient as it determines ... future adjustments to the target range for the federal funds rate”, despite acknowledging that “the labour market remains strong and economic activity rose at a solid rate”.2 As of 3 May, the Federal Funds futures curve is pricing in two rate cuts before April 2020.3

This drastic reversal illustrates that the Fed under Powell understands just how important accommodative monetary policy has been to this long bull market, and as such, may be unwilling to stomach the volatility that the end of the cycle will inevitably bring.

The Trade Deal Put – ‘Tariff Man’ or ‘Epic’ Deal?

The second put is the tone, albeit dualistic, of the ongoing US- China trade negotiations.

In 2018, US President Donald Trump was consistently aggressive in the tone of his communications toward China, demanding greater access for US companies, agricultural goods, an end to forced technology transfer and intellectual property theft. The high water mark was probably a 4 December tweet, in which Trump referred to himself as “a Tariff Man” and said “When people or countries come in to raid the great wealth of our Nation, I want them to pay for the privilege of doing so”. He has also touted the need for a comprehensive “real [trade] deal with China or no deal at all”.4

In the first few months of 2019, the aggression turned somewhat muted. Trump instead focused on the positive progress in negotiations, promising that a trade deal will be “massive”, “epic” and that “Big progress [is] being made on soooo many fronts”.

This optimism was short-lived. In May, Trump doubled tariffs on USD200 billion worth of Chinese imports, which China answered with duties on USD60 billion of American goods. Market moves in the immediate aftermath of these announcements showed that it appeared to have been pricing in a deal.

Our view is that it may be worth focusing on Trump’s need for political victories ahead of the 2020 election. Based on his past record5, it would be no surprise if a completed trade deal – even one that failed to comprehensively resolve the issues around subsidies and intellectual property – was presented as a ‘victory’. Indeed, Trump has been sensitive to the moves in the financial markets and is at pains to provide reassurance, stressing that trade “conversations into the future will continue” and that his “respect and friendship with President Xi is unlimited”.6 With this in mind, we expect a deal to be signed and then be praised as masterful statecraft, irrespective of its final contents.

The Brexit Put

The third put is the repeated delay by the British government to implement Article 50, now postponed to 31 October from the original date of 29 March. Prime Minister Theresa May’s government seems paralysed, both terrified of the prospect of leaving without a deal and unable to rally support for the Withdrawal Agreement. Ongoing negotiations with the opposition Labour party have, at the time of writing, produced no consensus.

This short-term Brexit put has been highly effective: 6- month implied sterling volatility has collapsed since the March delay7 and short interest in UK domestically exposed equities has fallen from 5.5% of share capital in January 2018 to 2% currently.8

So, the Brexit delay put has been an excellent sticking plaster for short-term volatility, and may continue to be so – until 31 October at least.

(Note: This was written before Theresa May announced her decision to step down on 7 June. Our underlying thesis still stands.)

The Italian Budget Put

There has been precious little coverage of the Italian budget since December 2018, when a deal – to limit the amount by which Italy violated the EU’s budgetary rules – was agreed between the EU and the Italian government.

The disagreement over the Italian budget caused the spread between BTPs and bunds to reach a high of 326 basis points on 18 October9, a spike with potentially dangerous consequences for the Italian banking system. The subsequent ratification deal eased this pressure. Italy was allowed to continue to run a national debt of 132% of GDP10 (in breach of the EU’s 60% target), in return for a reduction the overall target budget deficit from 2.4% to 2.04% of GDP.11 The Italian government’s growth assumptions were also reduced from 1.5% to 1.0%.

Italy was in recession when the deal was struck.12 If the Italian economy was already shrinking, the 1.0% growth assumption which created the 2.04% forecast budget deficit was already incorrect, which meant that Italy was in breach of the deal almost before it was ratified!

In the first quarter of 2019, Italian GDP rose 0.2%, slightly above market expectations, but below the rate of growth needed to achieve budgetary targets.13 However, the EU has since shown little appetite for renewing the confrontation, despite the worsening trajectory of Italian government debt, which is not negligible – Italy has the sixth-worst debt-to-GDP ratio in the world14 and, in our view, constitutes a systemic risk.

Again, stability has been prioritised above fiscal discipline: at a time of unprecedented challenge to its union and ahead of the EU elections, the union has – understandably – shown itself to be more committed to placating the Italian government than enforcing its own rules. Politically, the Italian put on volatility is entrenched for the long term, in our view.

The ‘Icarus’ Put

For a man who thinks the French President should resemble Jupiter, Emmanuel Macron is doing a much better impression of Icarus. As the wings of his reform agenda melt in the heat of the gilets jaunes’ petrol bombs, Macron seems to be grasping at political concessions as a means of breaking his fall to earth.

It is worth considering the ambition of Macron’s manifesto. His presidential election platform vowed to cut the number of civil servants by 120,000, make EUR60 billion of budget savings, reform pension schemes, cut corporation tax, remove the wealth tax and implement reforms to improve the flexibility of the labour market. He also had some success: as we noted in ‘Macron: Reasons to Believe’, he was able to implement labour market reforms and repeal the wealth tax. However, we also said that the most difficult hurdles stood ahead of him.

Indeed, the success of the repeal of the wealth tax lay some of the seeds of the violent volatility that would soon engulf France: the combination of tax cuts for the rich and an increase in diesel fuel duty sparked popular protests against him as a president of the wealthy. Resulting concessions by Macron – which could total about EUR25 billion when cancelled planned tax hikes and various tax reductions are taken into consideration – have bought breathing space and relative stability.

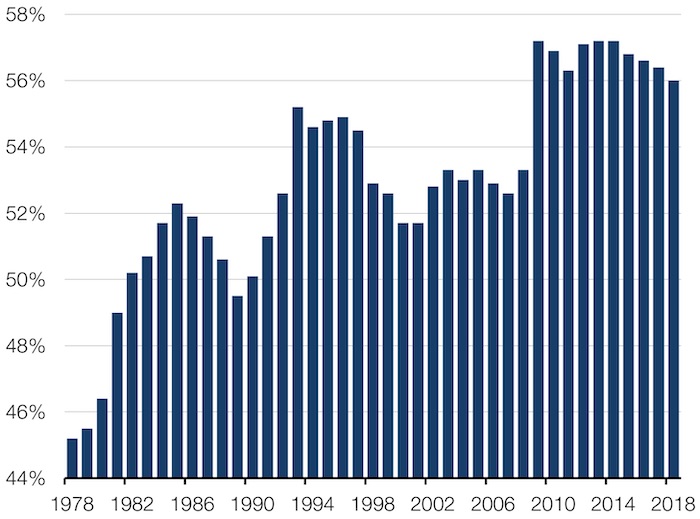

Again, we see this as a longer-term put. In France, the most pressing issue is still the needed reform of the French public sector. As of 2018, government spending accounted for 56% of French GDP (Figure 1). Reforming the public sector has historically not been easy, with previous attempts under Jacques Chirac and Alain Juppe failing in 1995.

However, the reform of the French state has now been abandoned and without it, the trajectory of the French economy looks dispiritingly similar to before Macron took office.

Figure 1: France Government Spending to GDP

Source: Trading Economics; as of 2018.

The Socialist Put

The final put is the recent stimulus applied to the Chinese economy. To use BCA Research’s phrase, this is the ‘socialist put’, best summarized as credit creation on an industrial scale.

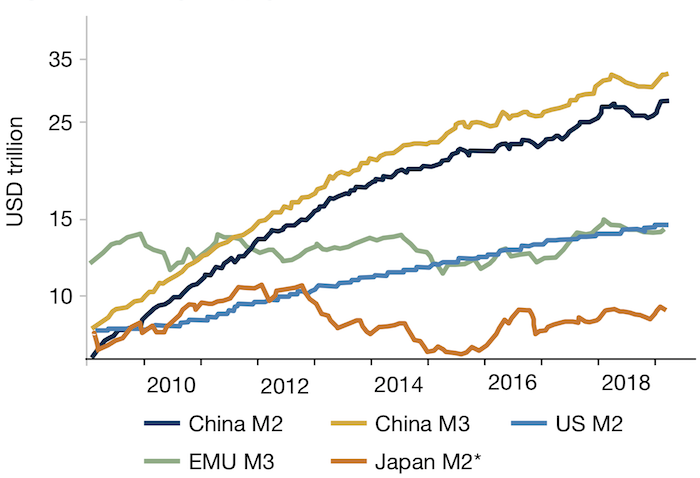

We have previously noted that the recent stimulus is small compared to previous Chinese credit injections, and have also pointed out the terrifying, disproportionate scale of credit creation in China since 2008(Figure 2). We are certainly not the first, and won’t be the last, to note that dealing with the legacy of this debt may be a long-term problem for China.

Figure 2: Money Supply Levels

Source: BCA Research. As of April 22 2019. *Includes certificates of deposit.

The most recent bout of stimulus shows that the policy toolbox of the Chinese government and People’s Bank of China (PBoC) remains limited, despite positive soundbites over the last few years. Zhou Xioachuan, Governor of the PBoC, stated in October 2017 that China was approaching its Minsky Moment, a sudden collapse of asset prices created by debt or currency pressures.15 President Xi Jingping urged companies to reduce their debt levels in 2018.16 Yet, when faced with slowing growth in late 2018 and early 2019, China instead chose to double down on its previous policy and expand the creation of credit. On top of that, we have seen the Chinese government stepping into equity markets to stabilise prices, another put for investors.

Conclusion

The stock market’s turnaround since December has, in our view, been driven by the refusal of global policymakers and politicians to embrace volatility. The most worrying feature is how reliant Italy, France and China are on debt and deficits. We see only two ways out of this debt: a productivity shock; or more likely, printing even more money. It is thus no surprise that talks about ‘Modern’ Monetary Theory have flared up recently.

1. https://www.cnbc.com/2018/10/03/powell-says-were-a-long-way-from-neutral-on-interest-rates.html

2. Source: 1 May FOMC statement.

3. Source: Bloomberg.

4. https://twitter.com/realDonaldTrump/status/1070110615627333632

5. https://twitter.com/realDonaldTrump/status/1079900120047603713

6. https://twitter.com/realDonaldTrump/status/1128257891805298690

7. Source: Bloomberg

8. Source: Morgan Stanley; as of 10 May 2019.

9. Source: Bloomberg.

10. https://tradingeconomics.com/italy/government-debt-to-gdp

11. Source: BBC; https://www.bbc.co.uk/news/world-europe-46620853

12. https://tradingeconomics.com/italy/gdp-growth

13. https://tradingeconomics.com/italy/gdp-growth

14. href="http://worldpopulationreview.com/countries/countries-by-national-debt/

15. http://worldpopulationreview.com/countries/countries-by-national-debt/

16. https://www.business-standard.com/article/international/xi-jinping-urges-local-govt-and-state-owned-enterprises-to-reduce-debt-118040301239_1.html

You are now exiting our website

Please be aware that you are now exiting the Man Institute | Man Group website. Links to our social media pages are provided only as a reference and courtesy to our users. Man Institute | Man Group has no control over such pages, does not recommend or endorse any opinions or non-Man Institute | Man Group related information or content of such sites and makes no warranties as to their content. Man Institute | Man Group assumes no liability for non Man Institute | Man Group related information contained in social media pages. Please note that the social media sites may have different terms of use, privacy and/or security policy from Man Institute | Man Group.